China's economic data for the first half of the year are being released in succession, indicating the resilience of the world's second-largest economy to the impact of the COVID-19 pandemic, as well as the effectiveness of the Chinese government's various bailout policies. Researchers at ANBOUND believe the signals from China's economic juggernaut will catch the attention of global markets as the pandemic continues to engulf the world. As always, China's economic international influence will go far beyond geopolitical influence.

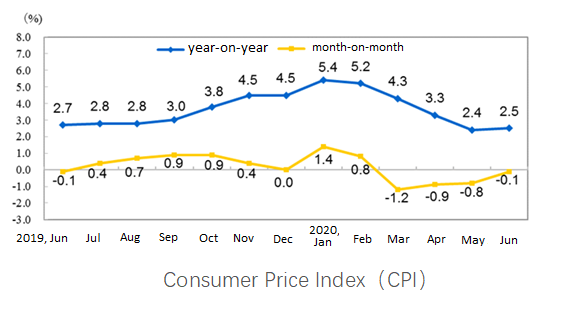

The initial set of economic data to be released for the first half of the year is the price index, namely the consumer price index (CPI) and the producer price index (PPI). The National Bureau of Statistics announced on July 8 that China's CPI rose 2.5% year-on-year in June. By category, urban inflation was 2.2% and rural inflation was 3.2%; food inflation was 11.1% and non-food inflation was 0.3%; goods inflation was 3.5% and service inflation was 0.7%. In the first half of 2020, China's CPI rose 3.8% year-on-year.

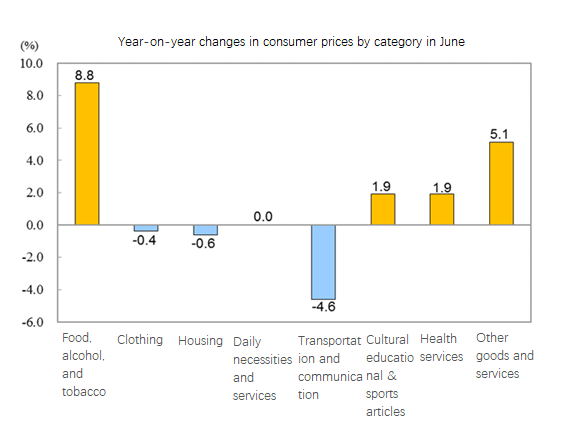

In terms of changes in the price index, CPI growth in the first half of the year has slowed significantly compared with the beginning of the year. In June the CPI growth of 2.5% is a very moderate and normal price level. However, looking at the structure of the CPI, there are certain issues. In June, the prices of food, tobacco, and alcohol rose 8.8% year-on-year, contributing about 2.64 percentage points increase in the CPI. This means that if food, tobacco, and alcohol were excluded, the CPI will be negative in June. Breaking it down further, the price of meat and livestock rose by 57.4%, contributing about 2.61 percentage points increase in the CPI; of which the price of pork rose by 81.6%, contributing about 2.05 percentage points increase in the CPI. Among other prices, prices of other goods and services increased by 5.1%, while those of cultural educational and sports articles and health services all increased by 1.9%. Prices of daily necessities and services remain flat; transportation and communications, housing, and clothing prices fell by 4.6%, 0.6%, and 0.4%, respectively.

As can be seen, the changes in CPI in the first half of the year are generally mild, but the structure is very different, mainly due to the rise of food prices, especially the rise of pork prices pushed up the CPI. In fact, domestic economic activity has been generally suppressed under the pandemic, and prices of many goods and services are falling. Two problems can be reflected here. First, the rising CPI reflects the same old problem of last year. i.e. the huge rise in pork prices has exerted a strong influence on the overall price, apparently "masking" the impact of the pandemic. Second, the COVID-19 outbreak has hit the economy, with a relatively obvious contraction in production and consumption activities.

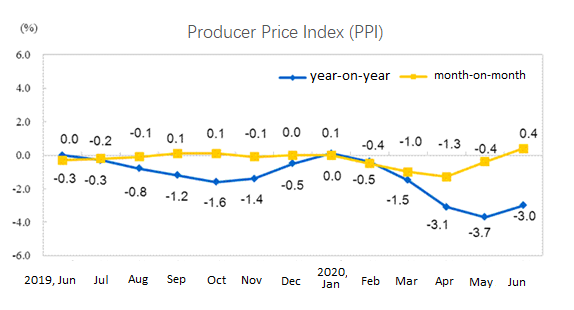

In terms of industrial prices, in June 2020, the PPI fell by 3.0% year-on-year and the purchasing price index for industrial producers dropped by 4.4% year-on-year. In the first half of the year, PPI dropped 1.9% and the purchasing price index for industrial producers dropped 2.6%. Among producer prices, the price of means of production fell by 4.2%, contributing to the overall drop by about 3.11 percentage points. Among the purchasing prices of industrial producers, the prices of fuel fell by 14.2% year-on-year; the prices of chemical raw materials fell by 9.4%; the prices of non-ferrous metals and electrical wires fell by 3.3%; the prices of ferrous metals fell by 2.2%; the prices for agricultural and sideline products rose 5.8%.

This indicates that with the recovery of industrial production, PPI began to show a slight rise, which is roughly consistent with the positive growth of industrial added value and positive growth of industrial profits in the second quarter of this year. Given the global economic downturn, China's resumption of work and production cannot stand alone. The recovery of domestic industrial production will continue to be weighed down by shrinking international demand. Unless massive domestic infrastructure investment is restarted, creating a strong incentive for infrastructure construction, otherwise, the industrial producer prices are unlikely to rise significantly. In fact, this year's emphasis on "new infrastructure", as opposed to conventional infrastructure, may have a different price pull for the industrial sector.

It should also be noted that among the challenges facing China's economy in the second half of the year, a new risk is emerging, that is the widespread flooding in southern China. At present, most parts of the southwest, central, south, and east China have been directly affected by floods. Besides the loss of lives and property, the impact of the flood on agriculture and food production cannot be ignored. If this year's autumn grain production is affected, it is likely to cause food prices to rise. It would not be good news for China's economy if food prices rise as the economy struggles to recover. In addition, the flood will also have a certain impact on industrial production. The industrial recovery after the pandemic has just improved, and now it is experiencing floods again, which may affect economic recovery in the second half of the year.

Final analysis conclusion:

Price data for the first half of the year reveals that China's economy has shown a relatively stable recovery after the pandemic, but the impact of the pandemic on services and consumption is still evident. The economic recovery in the second half of the year is still facing uncertainties in domestic and international markets, especially the floods in the southern region are posing new risks.