For the first quarter of 2024, optimism is increasing in the market regarding the performance of the Chinese economy. Apart from a few international rating agencies like Fitch Ratings being concerned about the worsening debt situation in China, most institutions tend to believe that the first quarter of the Chinese economy may achieve a good start. Positive news includes a 4.2% year-on-year increase in national fixed asset investment for January and February 2024, a 7.0% year-on-year increase in the value added of industrial enterprises above designated size for January and February, a 5.5% year-on-year increase in total retail sales of consumer goods for January and February, and an 8.7% year-on-year increase in the total value of imports and exports for January and February. Among them, exports grew by 10.3% and imports by 6.7%.

However, researchers at ANBOUND believe that despite the recovery momentum of China's economy in the first quarter, caution should still be exercised. Looking at the performance of domestic prices in March, over-optimistic expectations should not dominate the assessment on the matter.

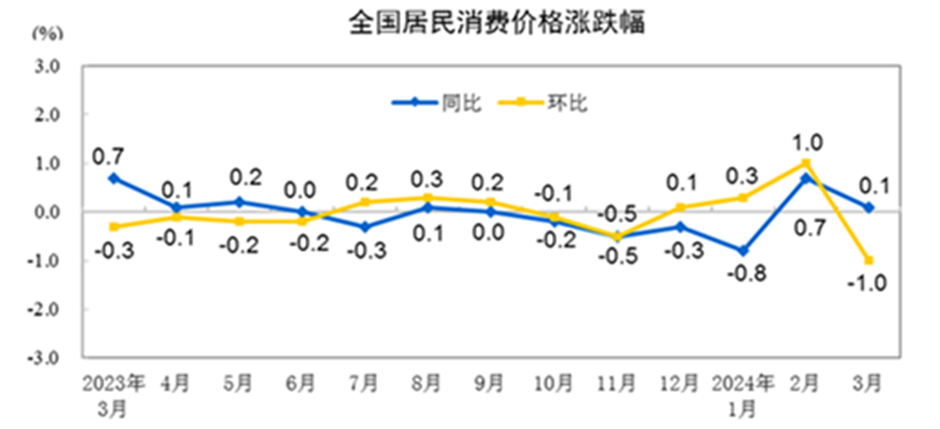

Data released on April 11 by the country's National Bureau of Statistics (NBS) show that in March 2024, the national consumer price index (CPI) rose by 0.1% year-on-year. Among them, urban areas remained flat, while rural areas rose by 0.1%; food prices fell by 2.7%, non-food prices rose by 0.7%; consumer prices fell by 0.4%, and service prices rose by 0.8%. On average for January to March, the national consumer price index remained flat compared to the same period last year. In March, the national consumer price index fell by 1.0% month-on-month. Among them, urban areas fell by 1.0%, rural areas fell by 0.7%; food prices fell by 3.2%, non-food prices fell by 0.5%; consumer prices fell by 0.9%, and service prices fell by 1.1%. The year-on-year increase in the CPI in March fell back, mainly affected by the decline in food and travel service prices. The year-on-year decline in food prices in the month increased by 1.8 percentage points to 2.7%, dragging the CPI year-on-year decrease by about 0.52 percentage points, with a downward impact increase of about 0.35 percentage points compared to the previous month. After the Spring Festival, seasonal weakening of food and travel service prices dragged the month-on-month CPI from a 1.0% increase in February to a 1.0% decrease, the lowest since April 2020.

Figure 1: National resident consumption in China

Source: National Bureau of Statistics

Researchers at ANBOUND believe that in March, following the Spring Festival, China's economic activity has returned to normal, with the year-on-year growth of the CPI slowing to 0.1%, barely positive, and a significant month-on-month decrease of 1.0%. This actually indicates that normalized real consumption activity, after seasonal adjustments, is not as optimistic as imagined by some institutions.

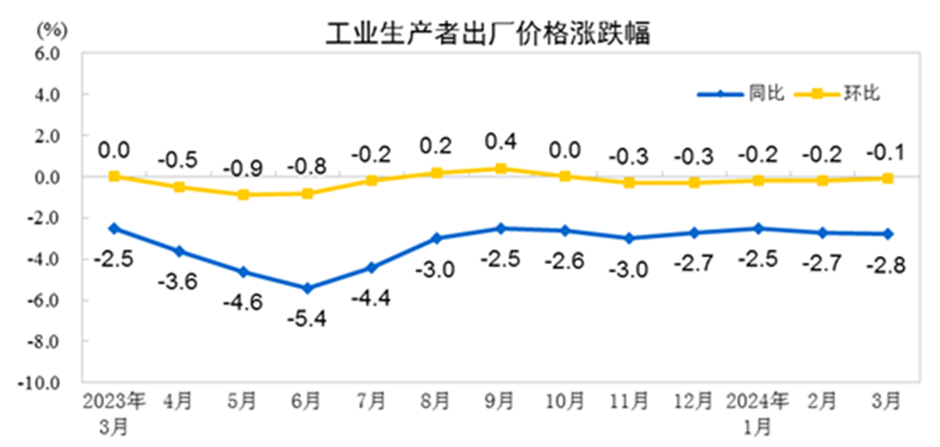

Looking at the changes in the producer price index (PPI), in March 2024, the national PPI fell by 2.8% year-on-year and decreased by 0.1% month-on-month; industrial producer purchasing prices fell by 3.5% year-on-year and decreased by 0.1% month-on-month. In the first quarter, industrial producer ex-factory prices decreased by 2.7% compared to the same period last year, and industrial producer purchasing prices decreased by 3.4%.

Figure 2: PPI in China

Source: National Bureau of Statistics

The price of production materials dropped by 3.5%, affecting the overall PPI level to decrease by approximately 2.58 percentage points. Among them, the prices in the mining industry fell by 5.8%, raw material industry prices dropped by 2.9%, and processing industry prices decreased by 3.6%. Meanwhile, consumer goods dropped by 1.0%, affecting the overall PPI to decrease by approximately 0.26 percentage points. Food prices decreased by 1.3%, clothing prices rose by 0.3%, general daily necessities prices decreased by 0.1%, and durable consumer goods prices decreased by 1.8%.

It can be seen that the PPI in March still maintained a stable decline. The year-on-year decrease in the PPI in March was 2.8%, the lowest in four months since December 2023, and continued to decline compared to February, when the Chinese New Year occurred. Observing the window where the PPI decline rate is slowly increasing, one can deduce that the industrial production activity in March is still relatively sluggish. This does not match the upward trend shown by previous fixed asset investment data.

Why is there often a gap between the actual performance of the Chinese economy and expectations? Researchers at ANBOUND believe that this may be related to the understanding of the Chinese economic system by policy departments and their views on economic regulation.

We believe that the Chinese economy is an extremely complex and massive system with strong inertia. When it is in a phase of rapid growth, it is difficult to suddenly slow down the speed of the economic system; and once the economic speed slows down, it is also very difficult to accelerate again. It not only requires significant resource input but also takes a considerable amount of time. Therefore, the key to macroeconomic regulation of the Chinese economy is not to adopt drastic policies like heavy intervention, or tight constraints. The fact of the steep decline in China's economic growth over the past few years and the back-and-forth changes in economic regulation, along with a significant number of synthetic fallacies, are in some ways lessons learned.

The Chinese economy, as a vast and complex system, is fundamentally a market economy. While there is the role of government regulation and the significant impact of policies, ultimately, its operation relies mainly on market mechanisms and forces. The key to successful macroeconomic regulation in China lies in coordinating both the visible hand with the invisible hand, minimizing the boom and bust cycles as much as possible.

The CPI and PPI in March are just one window to observe the Chinese economy. However, they indicate that the Chinese economy is still in a challenging phase of gradual recovery. Factors such as deglobalization and geopolitical turbulence continue to affect the global economy, while the structural adjustments of global industrial and supply chains are deepening. The expansion and tapping of the domestic market in China are also limited. In addition, from various aspects such as enterprise operation, labor employment, household income, and market expectations, the situation in China is still relatively fragile. Therefore, both policymakers and the market need to tread carefully and cautiously monitor the recovery of the Chinese economy in the first quarter.

Final analysis conclusion:

The CPI and PPI data for March show that the economic recovery in China is still in a weak momentum. Given the fragile recovery trend this year, both policymakers and the market of the country should handle the situation with care.