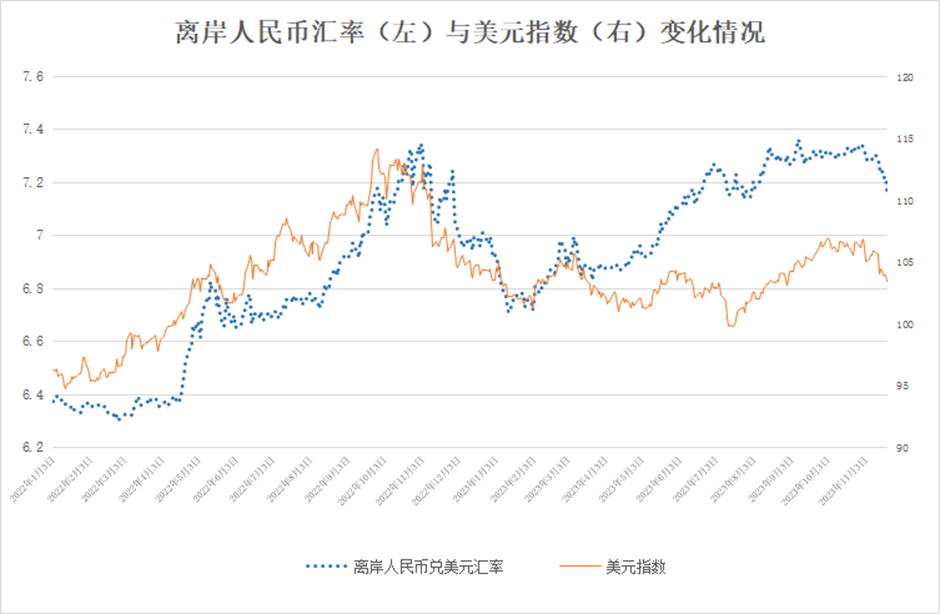

Since November 17, the exchange rate of the Chinese yuan (RMB) against the U.S. dollar (USD) has shown a strong rebound trend. By November 21, the onshore RMB-to-USD spot exchange rate rose above the 7.13 level at one point, closing at 7.1338, an increase of 409 basis points from the previous trading day, marking a nearly four-month high since July 27. Calculated based on the daytime closing price, the onshore RMB-to-USD spot exchange rate has accumulated an appreciation of 1127 basis points in the past two trading days, with a percentage increase of 1.555%. The offshore exchange rate, which reflects the expectations of international investors, has also risen for three consecutive trading days, with a cumulative increase exceeding 1.6% at one point on November 21, reaching a high of 7.1300. Moreover, for the first time since July, a situation has occurred where it leads the central parity rate. This continuous appreciation of the RMB reminds people of a similar situation last year when the offshore RMB exchange rate also rose rapidly from around 7.33 at the end of October to below 7 at the end of the year. The current offshore RMB exchange rate also reached a high of 7.34 at the end of October. In three weeks, it successively broke through the key levels of 7.20 and 7.15, reaching around 7.13, appreciating by nearly 2.8%. Under this similar trend, there is a significant possibility that the RMB exchange rate will return to around 7 for the year.

Figure: Changes in Offshore RMB Exchange Rate (Left) and USD Index (Right)

Source: Investing.com. Chart plotted by ANBOUND.

It is generally believed that the stabilization of China's economic situation since the third quarter, signals of stability in U.S.-China relations as indicated by the meeting between the two nations' heads of state, and the weakening expectation of the Federal Reserve’s interest rate hike have collectively driven the rebound of the RMB exchange rate. The meeting between the Chinese and U.S. leaders shows that the relations between the two countries are becoming stable, easing geopolitical risks. Its positive significance lies in the fact that although the bilateral competitive relationship has not been effectively eased, it is trending towards stability, reducing the uncertainty of worsening geopolitical competition for a considerable period. In addition, under the trend of the slowdown in the U.S. economy, the likelihood of the Fed continuing to raise interest rates has decreased. This has led to the decline of the U.S. dollar index, and the possibility of an expansion of the interest rate differential between China and the U.S. has diminished, which is favorable for the recovery of the RMB exchange rate. Researchers at ANBOUND have consistently believed that the changes in China's economic situation are the foundation determining the RMB exchange rate. The signs of stabilization in China's economy since the third quarter have become increasingly evident, laying the foundation for the stabilization and rebound of the currency’s exchange rate.

In the short term, some foreign institutions have raised their expectations for China's economic growth, prompting a certain amount of foreign capital to flow back into the Chinese bond market and, to some extent, increasing the demand for the RMB. Simultaneously, the increase in year-end foreign trade settlement demand has also driven the short-term demand for the Chinese currency, thereby causing the exchange rate to exhibit a cyclical rebound similar to last year.

Although the trend of the RMB exchange rate this year is similar to last year, there are significant changes on two fronts. Firstly, the economic situation has undergone substantial changes, and the country’s post-pandemic recovery process is rather complex, adding to the difficulty of economic expectations. Secondly, there have been significant changes in the foreign trade situation this year, with a prolonged period of negative growth in domestic exports. This situation has put greater pressure on the exchange rate compared to last year. Considering the short-term capital flow, the increased capital outflow in the second half of the year has led to the depreciation of the RMB. Additionally, the intensification of geopolitical competition between the U.S. and China has created a noticeable impact. This difference reflects a geopolitical risk premium for the RMB and signifies an increase in uncertainties regarding the trend of the currency.

It is worth noting that since the outbreak of the pandemic, the RMB exchange rate has repeatedly exhibited this roller-coaster trend, with shorter and more significant fluctuations. This has introduced considerable instability factors for both the Chinese economy and financial markets, even leading to some panic-inducing volatility. Based on recent years' experience, the fluctuation of the Chinese currency, whether appreciating or depreciating is detrimental to the country. The intensified depreciation of the RMB this year has not led to an improvement in exports. Conversely, the relative appreciation of the Chinese yuan has not attracted more direct investment. Instead, the capital flows generated by the fluctuation of the RMB have caused significant disruption to the Chinese capital market. Therefore, for China, ensuring economic stability and preventing systemic risks requires the stability of the RMB.

However, due to the fact that there are still both internal and external uncertainties, the RMB exchange rate is unlikely to form a trend expectation for quite some time and will continue to maintain a fluctuating trend. On one hand, although the Chinese economy has stabilized, and it is not impossible to achieve this year's 5% growth target, it still lacks sustained internal growth momentum. Risks in areas such as real estate have not been completely eliminated, which may have undesirable effects on economic stability. On the other hand, despite the stabilization of U.S.-China relations, this low-level stability is susceptible to disruption, and the premium of geopolitical risks will not disappear. In comparison, the positive impact of the shift in the Fed’s policy may become a secondary consideration. As mentioned by researchers at ANBOUND, the increase in uncertainties in the RMB exchange rate primarily stems from the changing expectations caused by shifts in the domestic economic fundamentals. In a situation where economic fluctuations intensify and uncertainties grow, predicting economic growth itself becomes increasingly challenging, leading to an increase in the cyclical fluctuations of the Chinese currency.

Final analysis conclusion:

The rapid rebound of the RMB exchange rate reflects the reduction of internal and external uncertainties affecting the Chinese economy. The expectations for this, however, remain unstable, and U.S.-China geopolitical risks are still high. These two long-term concerns imply that the RMB exchange rate will continue to experience cyclical fluctuations.