After achieving better-than-expected economic growth of 4.5% in the first quarter, China's economy has shown signs of slowing down in various economic indicators in April and May. This has raised concerns among many market participants about the direction of its economy. Some even suggest the risk of a "double-dip" recession, where the economy may experience a decline after a period of growth. Despite maintaining a relatively high year-on-year growth rate, the quarterly growth rate of the economy may decrease and even approach zero. The unstable outlook for the domestic economy has fueled pessimistic sentiment, resulting in a sluggish domestic stock market and a weakening of the Chinese RMB exchange rate.

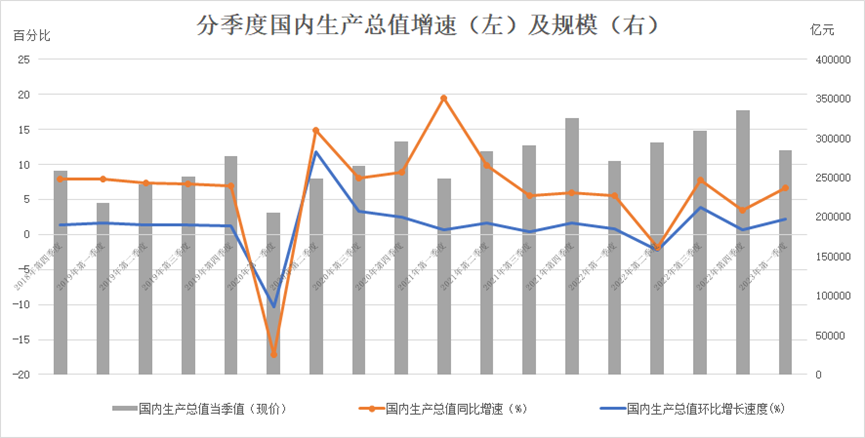

Figure: China’s Quarterly Gross Domestic Product (GDP) Growth Rate (left) and Scale (right)

Source: NBS. Chart plotted by ANBOUND.

Based on the situation in May, the current economic data shows a somewhat gloomy development, and there are many contradictory aspects, leading to significant divergences in expectations and judgments about the economy. On the one hand, the manufacturing PMI and services index, released by the country’s National Bureau of Statistics (NBS), both declined, indicating a continued decline in market prosperity. However, the services index still maintained a relatively high value, keeping the overall composite PMI on the optimistic side. The Caixin PMI differs from the official PMI in some respects. On the one hand, the Caixin manufacturing PMI unexpectedly rebounded above 50%. The May Caixin China Manufacturing PMI, announced on June 1, recorded 50.9, a 1.4 percentage point increase from April. The manufacturing new orders index rose above the critical point, reaching the second-highest level in the past two years. The employment situation in May further deteriorated, with the employment index dropping to its lowest level since March 2020. The Caixin China Services PMI for May recorded 57.1, a 0.7 percentage point increase from April, showing a further strong recovery in service industry activities. Currently, the optimistic situation reflected by the Caixin PMI contradicts the trend of the PMI released by the NBS, representing an uneven recovery among different economic components.

In addition, data shows that some significant indicators have also declined in May, indicating potential risks to the sustainability of economic growth. Firstly, the transaction volume of the real estate market has decreased while prices have fallen. In May, the average daily transaction volume of commercial housing in 30 major cities of the country showed a slight increase compared to April, and the year-on-year growth rate continued to be positive. However, the average price of newly built residential properties changed from an increase to a decrease, with a decline of 0.01% on a month-on-month basis and a further decline of 0.11% on a year-on-year basis. The average price of second-hand residential properties also experienced a decline, with a month-on-month decline of 0.25% and a year-on-year decline of 1.52%.

Secondly, offline consumption has experienced a decline after an initial high, with the overall growth rate slowing down. The average monthly number of moviegoers continued to increase in May, but the growth rate significantly dropped by over 40 percentage points to 13.3% compared to April. The year-on-year growth rate also decreased by over 60 percentage points to 301.0%.

Thirdly, there has been a decrease in inter-regional population movement. The passenger volume of subway transportation, after four consecutive months of month-on-month growth, declined in May with a 4.7% decrease compared to April. Among the 29 cities with available statistics, 25 cities experienced a month-on-month negative growth in subway passenger volume. In terms of air travel, domestic flights in Mainland China remained nearly the same as in April, while the month-on-month growth rate of flights to Hong Kong, Macau, and Taiwan decreased by over 20 percentage points to 3.6%, with the month-on-month growth rate of international flights decreased by over 45 percentage points to 22.4%.

Fourthly, the growth of car sales has slowed down. Looking at the weekly average sales volume of passenger cars from manufacturers' retail and wholesale data, there was a decrease in May compared to April, and the year-on-year growth rate is also declining.

Lastly, industrial production has weakened, with the overall capacity utilization rate of major industries such as steel, automobiles, and chemicals being lower than in April. The overall commodity price index and major raw material price index have also been declining. These situations indicate a potential slowdown in the month-on-month growth rate of the Chinese economy.

From the sluggish CPI data in April and other monetary and financial indicators, it can be observed that the current contradictions in the Chinese economy indicate that the economic recovery is not a comprehensive one, but rather a recovery in different sectors and economic components. These contradictions are also the main source of the current unstable expectations. If the Chinese economy achieves year-on-year growth in the second quarter, then the quarter-on-quarter data would still be higher than in the first quarter. Therefore, the notion of a "double dip" is somewhat overly pessimistic. Moreover, when considering the quarterly differences in the Chinese economy, measuring economic growth based on quarter-on-quarter growth rates has little significance. It is similar to the concern about deflation, which lacks practical meaning when the economy is still growing. This concern actually reflects a distortion between expectations and reality.

Researchers at ANBOUND have long pointed out that the Chinese economic recovery is a continuous and gradual process and will not rebound rapidly as many people hope. At the same time, the country’s economy not only faces the problem of insufficient demand but also encounters many structural supply issues. In particular, the contraction of the real estate market, which accounts for a significant proportion of economic activity, will inevitably drag down asset prices and exacerbate debt problems, thus having a negative impact on economic growth. This also means that the Chinese economy will not experience a rapid rebound in the situation of a sluggish and contracting real estate market, and is unlikely to achieve a comprehensive recovery after excessive contraction. Similarly, in a situation where the economy can still maintain growth, if deflation occurs, it not only signifies insufficient overall demand but also reflects short-term disturbances and does not necessarily represent the usual signals of an economic recession. Therefore, the weakness displayed by some data is a true reflection of this complex process and is also a signal of economic expectations shown in the capital market.

The current state of the Chinese economy is not as optimistic as expected, nor as pessimistic as some people imagine. It exhibits both strong resilience and shortcomings in terms of elasticity. There are both long-term issues and short-term factors at play. As pointed out by ANBOUND, China is still in a phase where it needs time to recuperate, and it lacks the foundation for stimulation and expansion. In the foreseeable future, on the one hand, the policy space is continuously narrowing, making strong stimulus less likely. On the other hand, the effects of loose policies are diminishing, which hinders economic structural adjustments because more resources are directed toward government investments with lower efficiency. In this situation, the key focus of macro policies should be on maintaining the sustainability of economic recovery, providing fundamental support to the economy, rather than pursuing rapid growth stimulation. To achieve more room for growth, a series of reform policies are needed to drive progress. Therefore, what the market needs more is an adjustment of expectations to adapt to the current state and trends of economic development.

Final analysis conclusion:

The PMI data for May and other economically significant indicators reflect a slowdown in the momentum of China’s economic growth. This is influenced by both cyclical factors and the imbalanced economic recovery. It also highlights the issue of inadequate endogenous driving forces in the economy following policy stimuli. Addressing these complex and contradictory economic dynamics goes beyond relying solely on economic stimuli. It necessitates the restoration of confidence and rejuvenation through comprehensive institutional and structural reforms.