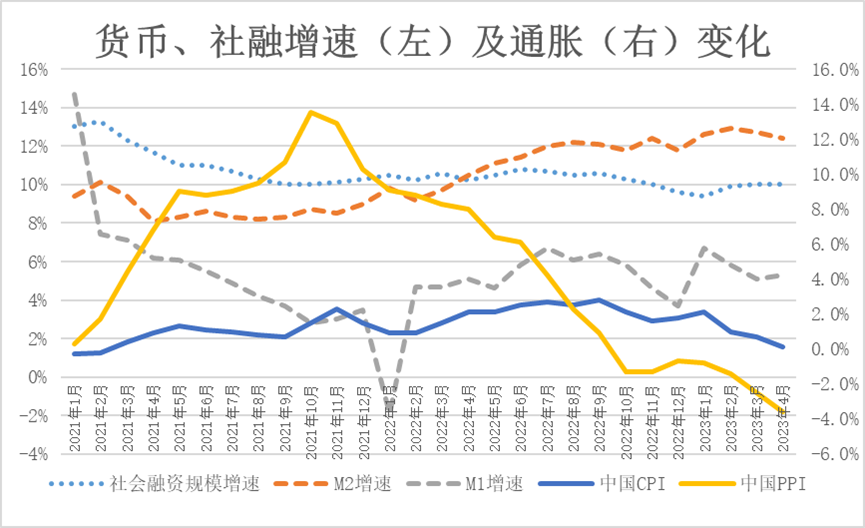

On May 11, a series of data, including inflation, money supply, and social financing, was released by the relevant authorities in China. According to the website of the National Bureau of Statistics (NBS), the Consumer Price Index (CPI) in April showed a 0.1% decrease month-on-month (MoM) and a 0.1% increase year-on-year. The core CPI, which excludes food and energy prices, shifted from unchanged to a 0.1% increase MoM and a 0.7% increase year-on-year (YoY), maintaining the same growth rate as the previous month. The YoY growth rate of CPI further declined from 0.7% in March. Similarly, the Producer Price Index (PPI) data paints a less optimistic picture. In April, influenced by factors such as fluctuations in international commodity prices, overall weak domestic and foreign market demand, and a relatively high base in the same period last year, the PPI showed a 0.5% decrease MoM and a 3.6% decrease YoY. Compared to the previous month, the PPI shifted from unchanged to a 0.5% decline on a monthly basis. In terms of YoY comparison, the PPI declined by 3.6%, expanding by 1.1 percentage points compared to the previous month. The widening of the YoY decline is primarily attributed to the higher base in industries such as petroleum and ferrous metals in the same period last year, as well as the recent weak domestic and foreign demand. Among them, the prices of production materials decreased by 4.7%, expanding by 1.3 percentage points, while the prices of consumer goods rose by 0.4%, indicating a decrease of 0.5 percentage points in the growth rate.

Figure: Changes in China’s Money Supply and Social Financing Growth Rate (Left) and Inflation (Right)

Source: National Bureau of Statistics, People’s Bank of China. Chart plotted by ANBOUND.

From the perspective of price changes, on the one hand, certain short-term factors such as significant fluctuations in energy and commodity prices have had an impact on inflation. However, at the same time, the consecutive decline in both the CPI and PPI, with the CPI approaching zero growth, indicates that overall domestic economic demand in China remains weak. This data confirms the previous predictions by researchers at ANBOUND that the lack of a driving force for economic growth and the difficulty of a rapid rebound are gradually becoming a reality. The decline in CPI suggests that the phase of releasing pent-up demand suppressed during the COVID-19 pandemic is nearing its end, and the domestic economy is bidding farewell to recovery-driven growth. The continuous decline in PPI indicates that there is not a strong demand for investment in the real economy. After a rapid recovery on the supply side, a structural contradiction of "supply exceeding demand" is emerging, as the recovery on the demand side is relatively slow. With the effects of the pandemic reducing, the long-term lack of market momentum will be the main challenge for the country’s domestic economic growth in the coming period. Its economy will not only need to undergo a process of demand recovery, but also face a process of structural reshaping.

The gradual decline in CPI data does raise concerns about deflation. Nevertheless, the core inflation, which excludes food and energy, remains at 0.7%, the same as in March, indicating that economic demand still exhibits resilience and there is room for improvement in the synchronization of supply and demand recovery after the fading of the pandemic factors. This also suggests that the possibility of deflation leading to an economic recession in the future is not significant. However, the insufficiency of demand recovery may be underestimated due to the low base effect, as the domestic economy is still likely to maintain a relatively high growth rate in the second quarter. Yet, the issue of inflation contradicts financial data. Looking at the monetary and social financing situation in April, although the M2 growth rate has slightly declined, it still remains at a high level, and the growth rate of social financing has remained unchanged compared to March. This situation indicates two possibilities for insufficient demand in the real economy. First, it may be due to a relative surplus state after the supply side's rapid recovery driven by policies. Second, structural issues in the economy continue to hinder economic development, especially the sluggishness of the real estate market, which still consumes a considerable number of financial resources.

From the perspective of monetary changes, as of the end of April, the M2 reached RMB 280.85 trillion, with a YoY growth rate of 12.4%. The growth rate was 0.3 percentage points lower than the previous month but 1.9 percentage points higher than the same period last year. M1 stood at RMB 66.98 trillion, with a YoY growth rate of 5.3%. The growth rate was 0.2 percentage points higher than the previous month and the same period last year. The rebound in M1 growth indicates that in the post-pandemic period, the business operations are still in the process of recovery, which is a positive sign. However, the decline in M2 growth, apart from factors such as a moderation in policy stimulus, also reflects a decrease in the activity level of financial operations and a decline in the efficiency of monetary fund utilization. This is still related to insufficient confidence and to some extent reflects the inadequate recovery of actual demand.

As of the end of April, the balance of RMB loans reached RMB 226.16 trillion, indicating a YoY growth rate of 11.8%. While the growth rate remained stable compared to the previous month, it was 0.8 percentage points higher than the same period last year. In April alone, RMB loans increased by RMB 718.8 billion, with a YoY increase of RMB 64.9 billion. Looking at the loan distribution by sector, household loans experienced a decrease of RMB 241.1 billion, among which there was a reduction of RMB 125.5 billion in short-term loans and RMB 115.6 billion in medium- to long-term loans. Conversely, loans to enterprises increased by RMB 683.9 billion, with short-term loans decreasing by RMB 109.9 billion, medium- to long-term loans increasing by RMB 666.9 billion, and bill financing rising by RMB 128 billion. It is worth noting that the increase in RMB loans during April fell significantly short of the market's expectation of over RMB1 trillion, and a substantial decline was observed on the MoM basis. This reflects the continued presence of policy support and the influence of seasonal factors. However, the growth rate of RMB loans remained unchanged from March, sustaining the upward trajectory in medium- to long-term credit driven by corporate investment demand. Simultaneously, there was a comprehensive decrease in household loans, indicating an asynchronous recovery between households and enterprises, limited confidence in future prospects, and a reluctance to increase leverage.

Additionally, there was a decline in RMB deposits observed in April. The RMB deposit balance at the end of April stood at RMB 273.45 trillion, marking a year-on-year growth rate of 12.4%. The growth rate was 0.3 percentage points lower than the previous month, and it was 2 percentage points higher than the same period last year. In the same month, RMB deposits decreased by RMB 4,609 billion, reflecting a YoY decrease of RMB 5,524 billion. Among the different categories, household deposits experienced a significant reduction of RMB 1.2 trillion, while non-financial corporate deposits decreased by RMB 140.8 billion. On the other hand, fiscal deposits increased by RMB 5,028 billion, and non-banking financial institution deposits increased by RMB 2,912 billion. The notable changes in deposits mainly originated from the substantial reduction in household deposits during April. It is noteworthy that, in contrast to the decline in corporate deposits and the growth in credit, both household deposits and loans exhibited a downward trend. Some of the reduction in deposits may be attributed to necessary daily expenses, while another portion may be influenced by the lingering lack of confidence in residential investment amid the downward trend in the real estate market. As households are still engaged in the process of repairing their balance sheets, their investment sentiment remains relatively weak.

In April, the data on social financing exhibited relative stability, but there is still a lack of upward momentum in social financing demand. As of the end of April this year, the stock of social financing stood at RMB 35.995 trillion, marking a YoY growth of 10%. The growth rate remained unchanged compared to March. Specifically, the balance of RMB loans issued to the real economy was RMB 22.44 trillion, with a YoY growth of 11.7%, which also remained consistent with March. Overall, the demand for financing continues to exhibit a resilient recovery pattern. Looking at the incremental changes in April, the total increment of social financing in April 2023 was RMB 1.22 trillion, which was RMB 272.9 billion higher than the same period last year. Among them, RMB loans issued to the real economy increased by RMB 443.1 billion, representing a YoY increase of RMB 72.9 billion. From the perspective of the open market, net financing through corporate bonds decreased by RMB 284.3 billion, a decrease of RMB 80.9 billion compared to the previous year. However, net financing through government bonds increased by RMB 454.8 billion, representing a YoY increase of RMB 63.6 billion. Domestic equity financing for non-financial enterprises decreased by RMB 99.3 billion, a drop of RMB 17.3 billion compared to the previous year. The performance of the securities market indicates a decline in corporate financing and an increase in government financing, which may suggest that the efficiency of investment activities and the market's investment returns are still not optimistic, and there is still a lack of quality investments. On the other hand, shadow banking activities have shown some level of activity. Among them, entrusted loans increased by RMB 8.3 billion, representing a YoY increase of RMB 8.5 billion. Trust loans increased by RMB 11.9 billion, a YoY increase of RMB 73.4 billion. Non-discounted bank acceptance bills decreased by RMB 134.7 billion, a decrease of RMB 121 billion compared to the previous year.

From the monetary and social financing data in April, as well as the changes in inflation, it can be seen that the Chinese economy is gradually recovering from the disruptions caused by the COVID-19 pandemic and returning to a more normal state. However, this normalcy implies that the long-standing imbalance between supply and demand will continue to hinder future economic growth and lack internal dynamism. The contradiction between inflation and financial data indicates that market participants have not fully regained their vitality after the impact of the pandemic. On the other hand, it also highlights the urgent need for China to improve structural distortions in the economy. It should be noted that under the policy model of "fiscal stimulus, monetary easing, and state-owned enterprise benefits", macroeconomic policies have limitations in improving the economy. While they may stimulate limited demand recovery, they could also exacerbate market distortions. The financial demand itself remains asynchronous and imbalanced. Future adjustments of the country to macroeconomic and microeconomic policies should focus on allowing the economy to recuperate, promoting effective recovery for both households and businesses. The Chinese economy not only requires further recovery in overall demand but also needs structural reshaping to unleash market vitality.

Final analysis conclusion:

In April, inflation in China continued to decline. At the same time, the growth rate of the broad money supply (M2) decreased while social financing remained stable. These conditions reflect the imbalanced state of the macroeconomy of the country during the post-pandemic recovery process, characterized by imbalances in demand and supply, consumption and investment, as well as financial and real sectors. In the coming period, the Chinese economy will need to address the dual challenges of demand recovery and structural reshaping.