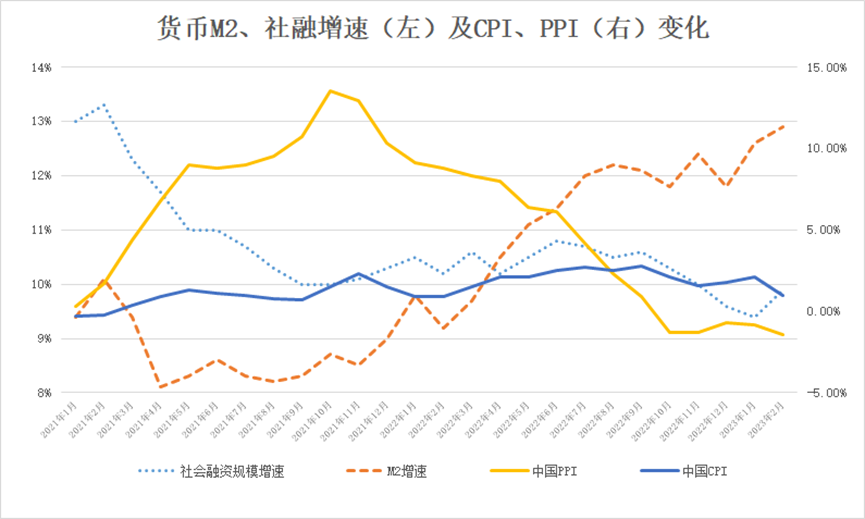

The financial statistics and social financing scale data released by the People's Bank of China (PBoC) in February indicate optimistic signs of China's economic and financial recovery. The data shows that the country's M2 grew by 12.9% year-on-year (YoY) in 2023, the fastest growth rate since April 2016; while M1 grew by 5.8% YoY, a slight decrease from the previous month. In February, RMB loans increased by RMB 1.81 trillion, a YoY increase of RMB 592.8 billion. Social financing grew by 9.9% YoY at the end of February, reversing the previous trend of continuous decline. In addition, social financing increased by RMB 1.95 trillion compared to the same period last year, an unexpected growth. According to researchers at ANBOUND, the recovery of monetary and social financing is partly due to the confidence brought by previous policy stimulus and partly due to the post-pandemic recovery of the economy itself. Under the driving force of endogenous power, the Chinese economy is continuously recovering, but the problem of insufficient demand means that the overall recovery remains unstable.

Looking at the monetary situation, although M1 sometimes falls, the growth rate of M2 has reached a new high in recent years. This is mainly due to the continuous growth of RMB loans. In February the loans increased by RMB 1.81 trillion, a YoY increase of nearly RMB 600 billion. This continued the good start in January, avoiding the unstable credit situation that occurred many times last year. It also indicated that the credit demand of market entities has recovered under the controlled situation of COVID-19. This is a good phenomenon for the improvement of the economy this year. This is especially true for short-term consumer loans, which have increased significantly YoY. In February, household loans increased by RMB 208.1 billion. Among them, short-term loans increased by RMB 121.8 billion, and medium and long-term loans increased by RMB 86.3 billion. Based on the calculations, they increased by RMB 412.9 billion and RMB 132.2 billion YoY, respectively. This indicates that consumption in the country has started to recover. In addition, medium and long-term loans for enterprises continue to maintain strong growth momentum, signifying that enterprise investment will still make a major contribution to the economy this year.

Figure: Changes in M2, Social Financing Growth Speed (Left), and CPI & PPI (Right) Changes

Source: PBoC, China's National Bureau of Statistics. Chart plotted by ANBOUND.

At the end of February, the balance of RMB deposits was RMB 26.82 trillion, a YoY increase of 12.4%, which was the same as the growth rate of the previous month and 2.6 percentage points higher than the same period last year. In February, RMB deposits increased by RMB 2.81 trillion, a YoY increase of RMB 270.5 billion Among them, household deposits increased by RMB 792.6 billion, non-financial corporate deposits increased by RMB 1.29 trillion, fiscal deposits increased by RMB 455.8 billion, and non-bank financial institution deposits decreased by RMB 516.3 billion. The deposit growth rate continued to maintain rapid growth. Firstly, the increase in derivative deposits derived from the enterprise side indicates an acceleration in the turnover speed of money; secondly, the precautionary deposits of residents still maintain a certain inertia, and the market confidence of the residents has not fully recovered. This also means that the recovery of the consumer market this year will be a gradual process.

In February, there was a rebound in the growth rate of social financing, which had been continuously declining in the past few months, indicating an economic recovery. The growth rate of social financing increased by 0.5 percentage points from January to 9.9%. This rebound suggests that credit has started to recover after the pandemic, which is a positive sign for market confidence. In February, the scale of social financing reached RMB 3.16 trillion, rare in recent years. This was due to an increase in loans of more than RMB 900 billion and an increase in government bond financing, reflecting the impact of policy promotion. Corporate bond net financing was RMB 364.4 billion, an increase of RMB 3.4 billion YoY. Government bond net financing was RMB 813.8 billion, an increase of RMB 541.6 billion YoY. Off-balance sheet items, such as undiscounted bank acceptance bills, decreased by RMB 7 billion, a decrease of RMB 415.8 billion YoY. This indicates that financing between enterprises is starting to recuperate, reflecting the gradual recovery of post-COVID market financial activities.

Financial data reflects an optimistic trend of economic recovery. However, looking at the overall situation from the perspective of supply and demand, the Chinese market still shows insufficient demand. In February, the YoY growth rate of the country's domestic CPI was only 1%, a significant decrease from January's 2.1%. Meanwhile, the extent of the decline in PPI has further deepened, reaching -1.4%, continuing to fall from January's -0.8%. Although short-term factors may interfere with price changes, the core CPI still reflects the situation of weak demand. Data shows that in February, the core CPI, which excludes food and energy prices, rose 0.6% YoY, a decrease of 0.4 percentage points from the previous month. Therefore, although financial and monetary data perform relatively optimistically, price data shows that the country's domestic demand has not fully recovered and is still under pressure from the supply side. As things stand, the Chinese economic structure still has some distortions. This also suggests that the economic recovery still does not have sufficient momentum and is more of a rebound. In addition, it acks the driving force of sustained growth.

Final analysis conclusion:

The monetary and social financing data for February indicates a gradual economic recovery in post-pandemic China. Nonetheless, sustaining this recovery remains uncertain as economic growth faces pressure from both the demand and supply sides.