In the three years since the outbreak of the COVID-19 pandemic, foreign trade has played a relatively important role in the Chinese economy. Affected by the pandemic, global production and supply chains were temporarily obstructed. At one point, China regained its important role as the "world factory" and its exports soared. This is especially true in 2021, where the contribution rate of net exports of goods and services to the country's economic growth reached 20.9%, driving GDP growth by 1.7 percentage points. Foreign trade contributed more to the economy than investment. In 2021, the contribution rate of gross capital formation to economic growth was 13.7%, driving GDP growth by 1.1 percentage points.

However, since 2022, the situation has reversed, and foreign trade in China has slowed down, even with monthly negative growth. On January 13, 2023, a press conference held by the State Council Information Office discussed the overall situation of the country's foreign trade in 2022. According to customs statistics, the total import and export value of China's goods trade was RMB 42.07 trillion in 2022, an increase of 7.7% over 2021, breaking through the RMB 40 trillion thresholds for the first time. Among them, exports were RMB 23.97 trillion, a year-on-year increase of 10.5%. Imports were RMB 18.1 trillion, a year-on-year increase of 4.3%. Judging from the annual data, both imports and exports have maintained positive growth, which seems to be all good. However, compared with the growth rate of foreign trade in 2021, it actually greatly slowed down. In 2021, the year-on-year growth of the country's import and export of goods, exports, and imports was 21.4%, 21.2%, and 21.5%, respectively.

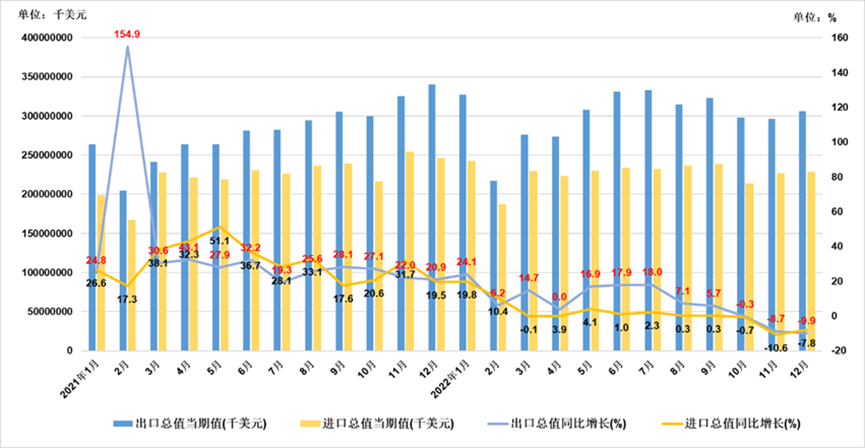

Figure 1: Scale and Growth Rate of China's Import and Export since 2021 (Monthly)

Source: General Administration of Customs of China. Chart plotted by ANBOUND

It appears that Chinese official institutions can always find optimism in any situation. Lu Daliang, a spokesperson of the General Administration of Customs, said that in 2022, China's total import and export value exceeded the RMB 40 trillion thresholds for the first time, and will continue to maintain stable growth on the basis of the high base in 2021, keeping the status of the world's largest trader of goods for six consecutive years. Among them, the total value of foreign trade increased to RMB 11.3 trillion in the third quarter, setting a new quarterly high. However, for enterprises, governments, and research institutions, it is more important to objectively view the changing trend of foreign trade and the risks that may arise in the future.

In the view of the researchers at ANBOUND, the development trend of China's foreign trade is far from optimistic. Judging from the situation in a single month in December 2022, denominated in RMB, the total import and export value of goods trade in December was RMB 3.77 trillion, a slight increase of 0.6% year-on-year, of which the export growth rate turned from positive to negative. The total export value decreased by 0.5% year-on-year %, and the total import value increased by 2.2% year-on-year. Denominated in the USD, the total import and export value of goods trade in December was USD 534.14 billion, a year-on-year decrease of 8.9%, of which the total export value decreased by 9.9% year-on-year, and the total import value decreased by 7.8% year-on-year. In fact, in the last three months of 2022, China's exports and imports have experienced negative growth in a row, with export growth of -0.3%, -8.7%, and -9.9% respectively; with import growth of -0.7%, -10.6%, and -7.8% respectively.

There is no doubt that China's foreign trade is facing a downward trend, and the role of foreign trade in boosting the country's economy has been weakened. Researchers at ANBOUND emphasize that this weakening is not only reflected in the change in the contribution rate of changes in net exports (i.e. surplus) to the economic growth rate in the statistical sense but also reflects the relationship between the Chinese economy and the rest of the world. The trend shows that the relationship between "Made in China" and the global supply chain has been continuously estranged.

Multiple factors have triggered changes in China's foreign trade. The first is the impact of the country's COVID-19 measures. Successfully in containing the virus in 2020 during the period of the novel coronavirus's earlier strains, China received a large number of overseas orders and its exports increased significantly in 2021. However, in 2022 the situation was reversed. The slowdown of the global pandemic has improved the world's production and trade situation, but China still adopted the strict "dynamic zeroing" policy and has been hit by several outbreaks throughout the year, seriously affecting its production and exports.

The second is the impact of the restructuring of the global supply chain. Under the waves of anti-globalization, the global supply chain began to adjust even before the pandemic. For example, Japanese companies have been considering the "China + 1" layout strategy for many years. The rise of Vietnam and other Southeast Asian countries in export processing and manufacturing is the result of the adjustment of the global supply chain. International frictions during the pandemic, as well as the impact of outbreaks of infection on China's manufacturing and foreign trade industries, have also exacerbated the relocation of the global supply chain from China. For some foreign investors, China is no longer a stable factor in the global supply chain, but a risk factor. For China to propose the "domestic circulation" model, it is on the one hand, to take advantage of the size of its domestic market, and on the other hand, to adapt to the trend of global supply chains alienating China.

The third is the impact of geopolitical factors. Geopolitical frictions have dominated the world in recent years. As a result, the free trade system and supply chain system formed in the era of globalization have been hit hard. In the era of traditional globalization, the low-cost "offshore manufacturing" model has been pursued. Under the influence of geopolitics, many "variants" of geo-manufacturing have emerged, i.e., friend-shoring manufacturing, near-shore manufacturing, and back-shore manufacturing. Future global industrial investment activities will have to take geopolitical factors into consideration.

Fourth, the global economic slowdown affects demand. With the global economy still affected by high inflation overseas (though the recent pressure of high inflation has eased), and the risk of recession in the world's major economies has increased, all these factors will hinder China's foreign trade growth.

Under the combined effect of these factors, one of the results is that a large number of manufacturing and trade activities will take place outside China, and some of them will be relocated out of China to overseas. Affected by this, The growth rate of China's foreign trade import and export will continue to slow down, and even show continuous negative growth.

After China relaxed its COVID-19 policy at the end of last year, many local governments in the country have organized production companies and foreign trade companies to go overseas to grab orders, retain orders, and expand markets. These efforts may have achieved certain results, but due to the trends affected by the factors mentioned above, there will be no possible means that can reverse the situation in the short term. If China wants to continue to maintain close ties with the world market, it may have to think about countermeasures from diverse aspects.

Researchers at ANBOUND believe that formulating specific countermeasures is technical policy work after having a clear strategy. As an independent think tank, we believe that in the face of various factors that are not conducive to China's foreign trade, the most important thing is to resolve strategic issues, accurately judge the situation at the strategic level, and formulate the correct strategy. In our opinion, there are two main points that China needs to grasp at the domestic strategic level:

The first is that China needs to adhere to reform and opening up, using it to guide the formulation of various policies. After more than 40 years of reform and opening up, China undoubtedly cannot return to isolation. In the game of geopolitics and geoeconomics, China should continue such a policy to break through the containment and decoupling imposed by other powers.

Second, China needs to carefully balance the relationship between its huge domestic market and the international market. What it needs to aim for is the drive for the country's industry and foreign trade, instead of slipping into only engaging in "domestic circulations". The long-term result of the internal circulation of any closed system is that the system's operating vitality will eventually be reduced, and gradually shrink in energy dissipation, leading to the downfall of the entire system. China had such an experience before, in its past development under the planned economic system.

Final analysis conclusion:

The continuous decline in China's foreign trade has sent warning signals to the country's foreign trade, overall economy, and economic policies. With this in mind, China needs to adhere to the basic national policy of reform and opening up to break through the containment imposed by the West, as well as balance the domestic market in its domestic-international dual circulations. This is with the objective that its own economy can always be integrated with the world to mutually drive the growth of each other.