With the holidays are approaching, it is time to reflect on what happened in 2022 and might happen in 2023. We are living in interesting times, as the Chinese saying goes, and that is not a good thing. I think we will look back on 2022 as the year in which geopolitics started to affect the economy in earnest.

Top of the list of events was the Russian invasion of Ukraine. Though US intelligence had been warning for this for some time, the number of troops Russia had amassed on the border—less than 200,000-- did not suggest a serious effort to conquer a country the size of France and Germany combined. Yet it happened.

The consequences are staggering. The suffering of the Ukrainian people stands out of course. Russia's cynical tactics after the offensive turned into a retreat means that slowly but steadily the country's infrastructure and housing is being destroyed by Russian artillery and air raids. Sadly, we have seen these gruesome tactics before in Syria and Chechnya with far less international uproar. The invasion, however, has far larger consequences.

It's geopolitics, stupid.

The geopolitical consequences of Russia's invasion are enormous. China continued its commitment to the "unlimited partnership" it signed with Russia just weeks before the invasion. In the eyes of many it meant it did not use the influence it had over Russia to affect the outcome of the war and that the country passed on an opportunity to demonstrate how international security in a multipolar world could look like. The Global Security Initiative that China proposed in the aftermath of the invasion is yet to gain any traction.

Much ink was spilled in the past year over what the invasion of Ukraine would mean for Taiwan. High level US military brass openly (and irresponsibly) talked about a possible invasion of Taiwan in 2023 or even sooner. The expansive military exercises of the PLA after Pelosi's visit added fuel to this perception.

More likely, though, is that whatever plans China had for Taiwan, the disastrous performance of the Russian military and the massive western response gives pause. As Arthur Kroeber of Dragonomics, a consultancy, put it: the risk of unprovoked action by China is still low, but the risk of provocations by the US on Taiwan is rising.

The US administration has been expanding its arsenal of China containment tools. These range from ineffective (such as IPEF) to aggressive, such as the recent semiconductor measures. The US has concluded that the best way to contain China is to cut it off from US—and allies'—technology.

According to Sullivan's speech in October that launched the measures, semiconductors are only a start, and it would not be a surprise if these are followed by measures in all technology areas in which China has declared it seeks to become a major player. In hindsight, publishing those plans in Made in China 2025 back in 2015 may not have been the best idea, and "hide your capabilities" as Deng Xiaoping ordered in the early 1990s seems pretty good guidance.

China's reaction to the semiconductor measures have thus far been muted. The measures that the US has imposed on China to ban (technically "licensing with presumption to deny") the sale of high-end chips produced with US technology or US personnel are far-reaching. Such measures are reminiscent of those imposed on the Soviet Union during the cold war or Russia today. According to the Global Times, China has taken the US to the WTO, as it argues the measures are in breach of the WTO charter. As noted before, there is a fair chance that an arbitration panel sides with China. Indeed, the WTO recently rejected the US tariffs on steel, including steel from China, that the US had imposed on national security grounds.

The WTO panel's conclusion clarifies that the GATT national security clause could not be invoked:

"In conclusion, the Panel does not find, based on the evidence and arguments submitted in this dispute, that the measures at issue were "taken in time of war or other emergency in international relations" within the meaning of Article XXI(b)(iii) of the GATT 1994. Therefore, the Panel finds that the inconsistencies of the measures at issue with Articles I:1 and II:1 of the GATT 1994 are not justified under Article XXI(b)(iii) of the GATT 1994."

The same conclusion could be drawn in the Semiconductor case that China is now bringing to Geneva. However, any appeal of the US would keep the case in limbo, as there is currently no functioning appeals body at the WTO, courtesy of the US.

Whether China will retaliate directly, say by cutting essential supplies to the US, remains to be seen, and largely depends on how US-China relations will evolve. China will no doubt double down on its program of indigenous innovation and dual circulation to reduce vulnerabilities. This will come at a cost, and may be less efficient than continued reliance on foreign supply and technology, but it will also be less secure.

Clearly, national security has come to play a larger role under Xi Jinping's domestic policies, even though, according to his report to the 19th CPC Party Congress, development is still the primary task of the party. More attention to national security is partly a reaction to the US trade and tech actions started under Trump, but maintained and extended under Biden. It is also because China's growing ambitions almost by necessity cause more friction with others, especially the leader of the free world. As Kevin Rudd expressed it, therefore "competition needs to be managed."

The geopolitical year ended on an upbeat note with a Biden-Xi meeting on the side lines of the Indonesia G-20 summit in Bali. Though details on that meeting remain scarce, it seems to have put a floor under a plummeting relationship. The agreement to continue discussions at working level on issues of joint interest are also encouraging, and a working level meeting has happened since. This may stop the downward spiral, for now, though Taiwan travel fever seems to be running high in the new House Republican leadership

For 2023 stabilization of the relationship with the US is China's government's main external challenge. Without it, the US will continue to intensify its containment policies, which would lead to a structurally lower growth path. Doing so in a year without Party Congresses or US elections, and before any chance of a return of a (more radical) Republican president is key for China's medium term prospects.

Geo-economics

Some of the economic damage is done, though. Geopolitics has now moved from the white boards of the corporate planning departments to the board rooms, and will affect investment decisions and consequently trade patterns going forward. The European Chamber of Commerce in China in its annual position paper warned of a "one world two systems," and their annual survey as well as that of AmCham's signal that more companies than ever have plans to shift at least part of their operations out of China. Some large ones such as Foxconn, producer of Apple phones and tablets, already have. Even Chinese companies seek safe havens to shield themselves of the impact of geopolitics as well as domestic politics.

Geopolitics, pandemic resilience, and greening of the economy will be powerful forces that will affect international supply chains. Economically, it means that there will be a move away from the "least costs" solutions that prevailed before. Increasingly, supply chains for the Chinese market will be domestic for critical goods, and predominantly regional for other goods. "Globalization is almost dead and free trade is almost dead. A lot of people still wish they would come back, but I don't think they will be back," said

Similarly, the US and Europe will try to "friendshore" or "near shore" their supply chains. While this may not happen overnight, this will be a future trend, and the process will not be smooth—and disruptive in some areas such as high tech. It will also accrue efficiency losses and cost pressures in the process, which seems a negative for the world economy as a whole. Morris Chang, founder of Taiwan Semiconductor Manufacturing Co expressed what many executives fear: "Globalization is almost dead and free trade is almost dead. A lot of people still wish they would come back, but I don't think they will be back."

A final economic fall-out from the Russian invasion is the accelerated move of western central banks to contain inflation. The price spike that the invasion caused worsened already bad inflation numbers, and threatened to become embedded in expectations. The rapid rate adjustments that followed cooled the US economy and strengthened the dollar, as the Fed moved first.

Like in the past, the adjustment in monetary policy also caused a reversal in capital flows for developing countries, many already badly hit by the COVID pandemic. Some are now facing problems in servicing their debt, including countries to which China has large exposures. Resolving this looming debt crisis based on the "Common Approach" agreed at the G20 is a top international priority for 2023, and one the US and China can agree on.

Politics trumped China's economics for most of the year.

Domestically, China's politics dominated its economics. The all-important 20th Party Congress took place in October, but dominated the whole year. The economic target of 5.5. percent was already outdated at the time of its pronouncement in March. The lockdowns of Shanghai, Shenzen and other economic hubs and the unpredictability of the "dynamic zero COVID policy" dragged down the economy, as did the unwinding of the real estate bubble after the "three red line" policy started to bite. But politics demanded stability, so the about-turn in both policies had to wait until after the 20th Party Congress.

The Congress itself brought little news in terms of policies or ideology, as the big shifts had already taken place at the 19th Party Congress in 2017. Neither was general secretary Xi Jinping's third term anything that was not expected by almost anybody. The big surprise was that Xi Jinping "ran the table" by removing any remaining diversity in the Standing Committee of the Politburo. While the anti-corruption campaign had already eliminated the "Shanghai gang," associated with Jiang Zemin, this time, the Communist Youth Faction around Li Keqiang suffered a complete removal from positions of power. Xi Jinping's core is now made up of people that are closely associated with him.

China's new leadership team has to face both new and old problems. Aside from COVID and the end of the real estate boom, it will need to address a host of long-standing economic challenges.

On the short term measures, the political coherence of the new team may be something of a plus, as the early days suggest. Soon after the conclusion of the 20th Party Congress, the government issued the 20 measures on COVID policy, which loosened the policy in a minor way. This was soon to be followed by the 10 measures, which initiated a major change in policies, including a move to quarantine at home, a vaccination campaign, the abolition of the PCR tests, and, more recently, the abolition of the travel passport. This shift came in the wake of widespread protests across the country and further weakening economic performance.

In the final month of the year, the government also moved more aggressively in addressing the property downturn. The supportive measures from the banks have de facto reversed the "three red line" policy, but it will take time for buyers' confidence to return. Moreover, structural factors such as demographics and slower urbanization may mean that this time is indeed different for the sector, and that China will end up with a smaller property sector compared to before. It will also be a different sector from before, with likely more rental housing and more social housing in the mix. So even those property developers that survived the storm may be less profitable than before. And local governments, which relied excessively on land sales, will remain cash strapped and more reliant on resuscitated local government financing vehicles.

How China will fare in the medium run depends on the reform path it takes.

China's potential growth rate for the coming 15 years could still top 5 percent or so. This is a number close to what Xi Jinping aspired to when he said that China's 2020 GDP could well double by 2035. While the country faces demographic headwinds, reforms in the retirement age could offset a considerable part of the projected labour force decline. Moreover, the people coming into the labour force are vastly better educated than those leaving it, which will increase productivity, as would relaxing the hukou system that would allow more people to move out of rural areas to more productive jobs in cities.

Financial sector reforms, including revamping better regulated fintech and better pension savings instruments would allow for a better allocation of capital as well. Reforms in the fiscal system could deliver a better revenue base for local government, and wean them off their excessive reliance of land sales and real estate development. Together, financial and fiscal reforms could cut over-investment in infrastructure and real estate and lead to higher and sustained growth.

Beyond the structural supply-side measures mentioned, China needs reforms to revamp demand, notably household consumption. The lack of robust consumption growth is increasingly becoming a constraint on China's growth. The recent changes in the COVID policy will gradually restore consumer demand. More needs to be done, including strengthening of the pension system and social safety net, which would lead to lower savings rates, and gradually increasing the household share in the economy, in particular through more pay-outs of corporate profits, which could also strengthen public finances.

On investor confidence, aside from the geopolitical challenges, China could restore confidence by clarifying its policy of "common prosperity" and by signaling that the ad-hoc regulatory crackdowns as we have seen in consumer tech are a thing of the past.

It is important to note that more consumption without concurrent supply-side reforms would just mean lower growth. A higher consumption share in the economy would lead to a lower investment rate (assuming government spending cannot be squeezed). This is fine as long as the remaining investments are better than before. This is a target-rich area in China where much of public investment in recent years was done to keep people at work, not necessarily to add productive assets to the economy. A cut in those investments, and reallocation of more investment to business investment (through a better financial sector) would do the trick. This holds even more so if the private sector, which has higher returns on investment than the state sector, gets a clear go-ahead signal from politics.

None of these reforms needed to return China to a sustainable growth path are incompatible with China's political direction. In fact, reforms could be well aligned with the New Development Philosophy, at least in principle. Next year is a good time to clarify how the two—philosophy and reforms, will be matched in the coming years.

The best way to do so is to prepare an economic policy plan in the coming year—and use the 3rd plenum of the 20th Central Committee for this purpose. One real miss of the last Xi term was that there was no Central Committee plenum dedicated to economic management—only one on the 14th Five Year Plan, the 5th Plenum.

The plans of the 3rd Plenum of the 18th Party Congress were clearly outdated by the time of the 19th Party Congress. Ideology and reality had shifted considerably by then, but a comprehensive statement of policy on how China's new directions (dual circulation, common prosperity, ecological civilization—now the "New Development Philosophy")—would translate into concrete policies has been sorely lacking. And uncertainty is an investor's worse nightmare.

So what does this all mean for 2023?

Much depend on how China's COVID policies will unwind, and this is very much a moving target. According to a model developed by China's most prominent epidemiologist, Zhong Nanshan, and his team, China is expected to return to pre-pandemic life by the first half of 2023, as Omicron will peak around the Spring Festival. Most expect a rebound of "revenge consumption" afterwards, but the transition to living with COVID will be a bumpy one, not least because of the abrupt change in policy itself.

A further important factor is the global economy. Export momentum has already weakened in the past semester, and the cooling world economy is not promising much for 2023—the US will barely squeeze out growth, and the EU is likely to face a recession. Notwithstanding China's increasingly close strategic alignment with Russia, economically it is a tiny market compared to the west, and hardly of significance except for its natural resources. So further decoupling, if it happens, will be a net loss for China in terms of external demand as well.

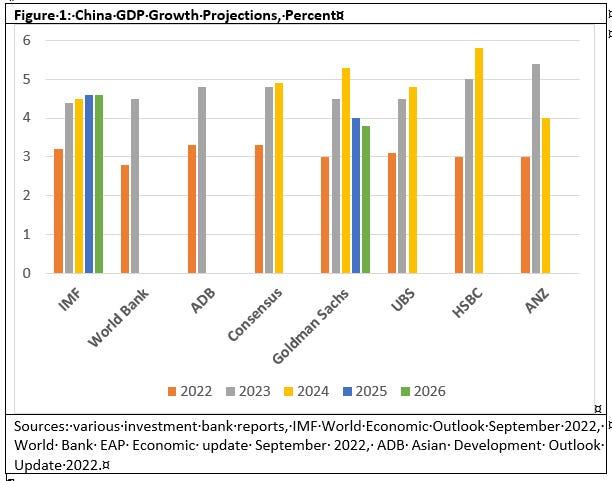

Given these uncertainties, projecting China's economic growth is an arduous task indeed, and one that yours truly happily leaves to professional forecasters. At the time of writing, the consensus forecast is 4.8 percent growth for2023, and a tad more for 2024. IMF, ADB and World Bank, which all made their projections before the COVID policy turned, are somewhat more pessimistic.

For the medium run, projections diverge more—largely following the degree of optimism on structural reforms. The optimists see a trajectory of growth returning to about 5 percent or more. Others, including the IMF and Goldman Sachs, see a post-COVID rebound, but then a levelling off to a more modest medium term growth rate well below 5 percent, compared to 6-7 percent pre-COVID.

Whatever next year may bring, I hope that you and your family stay healthy and safe and that you can do some good for others in the world. I wish you happy holidays and happy reading!

Sourced from https://berthofman.substack.com/p/202223?r=177zq&utm_campaign=post&utm_medium=email

Author:

Bert Hofman

Director, East Asian Institute

Professor in Practice, Lee Kuan Yew School

New Book: CPC Futures

https://epress.nus.edu.sg/cpcfutures/

Newsletter: https://berthofman.substack.com/