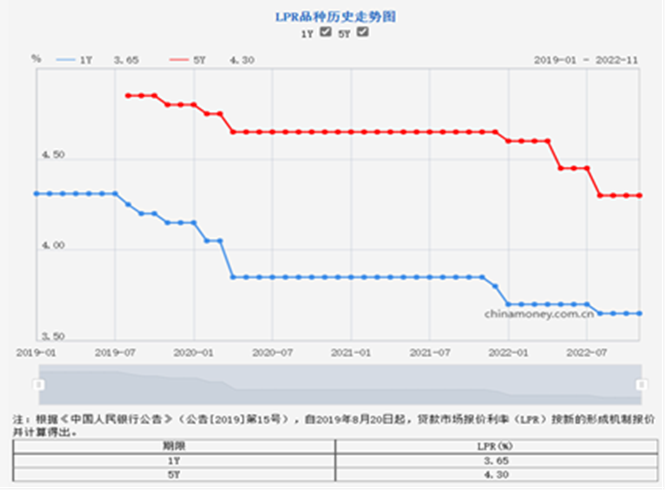

On November 21, the National Interbank Lending Center authorized by the People's Bank of China (PBoC) announced that the latest loan market quotation rate (LPR) is 3.65% for 1-year LPR and 4.3% for LPR over 5 years, both unchanged from the previous value. Previously, on November 15, the PBoC's medium-term lending facility (MLF) was RMB 850 billion), and the winning interest rate remained unchanged at 2.75%. This means that the pricing basis of LPR has not changed. As a result, most market institutions have expectations for LPR to remain unchanged as well.

Figure: China's LPR Trend

Source: China Money

So far, the Chinese LPR has "stood still" for three consecutive months. As far as the current situation is concerned, despite the slowdown in the economic growth trend and the increase in the demand of the real economy for the intensification of macro policies, the PBoC still adheres to a prudent monetary policy tone, which is far from the market's expectations. At the same time, the relative reduction of signals about easing in the PBoC's third-quarter monetary policy report means that the use of aggregate monetary policy tools will be more cautious. In this regard, researchers at ANBOUND tend to believe that it is unlikely that LPR will continue to adjust this year. The PBoC will return to a prudent neutral tone for a considerable period, and the focus of policy will be on structural policy adjustment.

In terms of the degree of "moderate liquidity easing", the growth rate of broad money M2 in China in recent months has continued to be higher than the growth rate of the social financing scale, which indicates that the real economy does not have a strong demand for money. Of course, this phenomenon, known as the "liquidity trap", comes mainly from the instability of physical demand. This is mainly due to the increase in uncertainties such as the COVID-19 outbreaks, which have constrained the expansion of demand. From the loan data, the new medium- and long-term loans to residents in October were only RMB 33.2 billion, the lowest since May this year, and an increase of RMB 388.9 billion less than the same period last year. As it stands, the previous LPR reduction has not been able to stimulate the recovery of the real estate market. Meanwhile, China's retail sales data for October and short-term loans to residents both reflect sluggish consumption at the residential end. In terms of enterprise demand, excluding state-owned assets and government departments, the demand of the private sector is also not optimistic. Under such constraints, a sustained push for monetary easing would not reverse expectations and generate incremental demand but would "increase future inflationary pressures". Although continued monetary easing is beneficial to capital markets, it has limited stimulus to the real economy, and sluggish demand is difficult to reverse by monetary policy alone, which will further increase financial bubbles. This is already reflected in the recent volatility in China's bond market.

As mentioned in certain media reports, China's LPR remains stable, which does not prevent financial institutions from increasing support for the real economy. According to the PBoC's monetary policy implementation report for the third quarter of 2022, the loan interest rate fell steadily, and the weighted average interest rate of corporate loans in September was 4.0%, down 0.59 percentage points year-on-year, at a low level since statistics began. Recently, the PBoC and other regulatory departments are increasing their supervision of commercial banks' lending, requiring large commercial banks to play the role of the leading exemplary. The strengthening of this administrative tool also shows that the PBoC's attention has shifted from "wide money" to "wide credit", and the effect of "window guidance" is stronger. The lack of policy momentum to continue reducing the LPR interest rate will also put commercial banks under more pressure.

It can also be seen from the central bank's continuous tapering of the MLF that the PBoC also tends to release short-term liquidity instead of using medium- and long-term policy tools to increase the flexibility and precision of liquidity adjustment. Yi Gang, governor of the PBoC, said a few days ago that from the perspective of economic operation effects, it is more appropriate to grasp the strength of China's macro policies. It not only strongly supports the stability of the overall macroeconomic situation but also maintains the basic stability of the price situation under the background of high global inflation. This also considers the internal and external balance. In this regard, the PBoC's evaluation of the effect of monetary policy implementation means that such a policy will remain in a relatively stable tone if there is not much change in the economic situation.

In addition, interest rates in China's domestic market are fluctuating and trending upward. Although the pace of interest rate hikes by the Federal Reserve will slow down in the future, the interest rate differential between China and the United States is still widening, and interest rates in the domestic market will adjust accordingly. Continued interest rate cuts will put more pressure on the stability of the RMB exchange rate. Looking at the new round of decline in the RMB exchange rate caused by the unexpected reduction of the LPR in August, maintaining the stability of the loan interest rate at a certain stage is also due to the consideration of maintaining internal and external balance.

Researchers at ANBOUND have mentioned previously that the PBoC can be expected to adopt relatively prudent policies, focusing on adopting targeted tools such as structural policies to promote "wide credit". Judging from the recent market operation of the central bank, the MLF tapering operation and the unchanged interest rates indicate a marginal narrowing of monetary policy, which is also implied in the third quarter monetary policy report. However, this does not mean a tightening of overall liquidity or a shift in the tone of monetary policy, but rather a shift in the focus of PBoC monetary policy. In the future, the strength of structural monetary policy will be increased, and the total goal of reducing comprehensive financing costs and maintaining moderate liquidity will be achieved with structural easing.

Final analysis conclusion:

China's LPR has been "standing still" for three consecutive months, which means that the use of aggregate monetary policy tools will tend to be cautious. Under the current internal and external situations, it is unlikely that the LPR will continue to adjust during the year. The PBoC will return to a prudent neutral tone for a considerable period, and the focus of policy will be on structural policy adjustment.