Not long ago, China's National Institute of Finance and Development (NIFD) released the country’s Q3 leverage ratio report for the year 2022. According to the report, the Q3 macro leverage ratio of the country increased by 0.8 percentage points to 273.9% in Q3, slower than the rise of 4.9 percentage points in Q2.

The recovery of economic growth in Q3 played a major role in stabilizing the macro leverage ratio, but according to researchers at ANBOUND, the change in the macro leverage ratio also reflects the decline in financing demand, which also means that the recovery of the overall economic demand remains sluggish. These cyclical changes mean that stabilizing demand will be the main challenge for China in the near future.

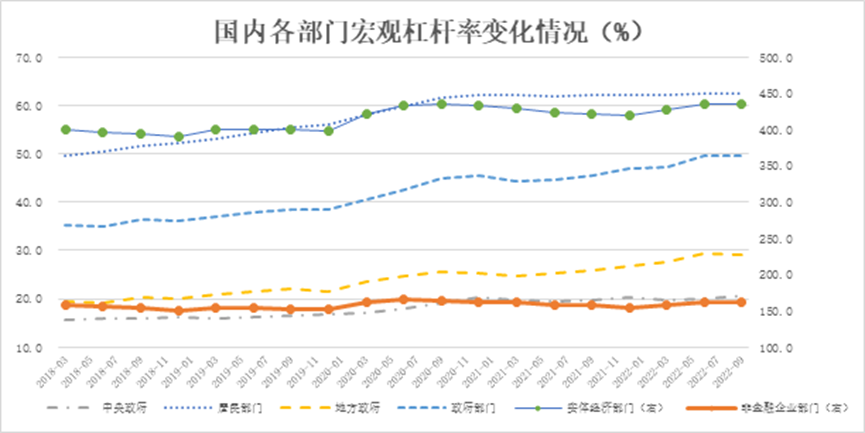

The residential leverage ratio increased by 0.1 percentage points from 62.3% at the end of Q2 to 62.4% in Q3 and increased by 0.2 percentage points in the first three quarters. Since the outbreak of the COVID-19 pandemic, the residential leverage ratio has fluctuated slightly at 62% for nine consecutive quarters. This not only reflects the limited increase in residential income, which restricts the demand for leverage but also indicates the decline in consumption, as well as the willingness to buy houses. All these signify that the recovery of domestic demand in China remains challenging. Data show that the growth rate of household debt in Q3 further dropped to the new low of 7.2%, with only personal business loans remaining at a high level of 16.1%. Some analysts believe that in an environment where the growth rate of total income is declining and economic growth is uncertain, the residential sector is more willing to take the initiative to deleverage. The growth rate of household consumption and the real estate transaction volume is relatively sluggish, which also limits the behavior of residents to increase leverage.

Figure: Changes in the Macro Leverage Ratios of Different Sectors in China (%)

Source: Research Center for National Balance Sheet, graph plotted by ANBOUND

The report shows that in the non-financial corporate sector, the leverage ratio increased by 0.5 percentage points in Q3, from 161.3% at the end of Q2 to 161.8%. The first three quarters increased by 7.0 percentage points, rising for three consecutive quarters, close to the level in Q1 of 2021. This is mainly due to the increase in the growth rate of medium and long-term corporate loans. Yet, the NIFD report also mentioned that the non-financial corporate sector is conservative in debt expansion, and the use of short-term papers to increase corporate loans in the first half of the year has also been suppressed. This is also closely related to the lack of investment demand.

Meanwhile, the leverage ratio of government sectors increased by 0.2 percentage points in Q3, from 49.5% at the end of Q2 to 49.7%, an increase of 2.9 percentage points in the first three quarters. Among them, the central government leverage ratio increased by 0.5 percentage points, from 20.1% at the end of Q2 to 20.6%, and increased by 0.4 percentage points in the first three quarters. The local government leverage ratio decreased by 0.3 percentage points, from 29.4% at the end of Q2 falling to 29.1%, an increase of 2.5 percentage points in the first three quarters. Seasonal changes in local government debt were the main factor behind the stabilization of the government leverage ratio in Q3. The peak of local government debt financing in the first half of the year has passed, and the newly issued financing in the second half of the year is limited, which led to a limited decline in the leverage ratio of local governments in Q3. This, in turn, has dragged down the increase in the government leverage ratio.

With consumption and private-sector investment demand weakening, most of the burden of boosting the economy falls on government investment and state-owned enterprise investment. Judging from the current situation, this poses a great hidden danger to the sustainability of the overall economic recovery. The NIFD report noted signs of "balance sheet recession" in both the residential sector and the non-financial corporate sector over the past two years. Although the cost of financing has fallen, the willingness to actively raise funds is not sufficiently strong; even a brief rise in revenue and profits will only further accelerate the speed of debt service and reduce debt, without increasing investment. Among all investments, the one that sees the most serious decline is in non-state-owned enterprises. In the first three quarters, the year-on-year growth rate of investment by private firms was only 3.4%, and the growth rate of investment by other limited liability enterprises was only 4.3% year-on-year. Most alarming in the corporate sector is the risk of a private economy's balance sheet recession. This is a typical feature of the financial cycle peaking and falling, and cyclical changes often bring serious financial and economic crises.

Changes in the leverage ratio structure in Q3 show that amid the triple pressures of demand, supply, and expectations, such shifts in expectations are affecting the behavior of both residents and enterprises, which may lead to a vicious circle between demand and expectations. Therefore, the slowdown in the growth of macro leverage ratios in Q3 is not all good news for stabilizing growth and preventing risks. The focus of stabilizing leverage will no longer be to prevent the leverage ratio from growing too fast but to avoid the decline of the macro leverage ratio caused by the recession of the balance sheet. With this in mind, the relevant authority will need to adjust the macro policies in considering the balance between demand, supply, and expectations. The focus needs to be on demand and expectations to avoid the collapse of the overall economy caused by changes in the financial cycle.

Final analysis conclusion:

China’s macro leverage ratio has tended to stabilize in Q3, which is beneficial for preventing financial bubbles and systemic risks. That being said, the cyclical changes in financial demand reflected by it have brought huge challenges to stabilizing growth. Hence, the country’s macro policies need to be adjusted in a counter-cyclical manner, so as to avoid vicious cycles formed by demand and expectations.