On October 24, China's National Bureau of Statistics (NBS) released the country's economic data for the third quarter of this year.

Based on preliminary calculations, the GDP for China in the third quarter of 2022 has increased by 3.9% year-on-year, up 3.5 percentage points from the second quarter. The accumulated GDP in the first three quarters of 2022 grew by 3% year-on-year, 0.5 percentage points higher than the first half of the year.

Judging from the economic growth data, this performance was higher than market expectations. According to Chinese news media Caixin's previous survey of the country's 14 domestic and foreign institutions, economists' forecasts for the year-on-year GDP growth rate in the third quarter averaged 3.6%, with a forecast range of 2.6% to 4.4%.

Figure 1: China's Year-on-Year Economic Growth (%), 2019 -2022

Source: NBS, chart plotted by ANBOUND

The recovery of economic growth in the third quarter of this year was mainly driven by the secondary and tertiary industries. In the third quarter, the added value of the primary industry increased by 3.4% year-on-year, 1 percentage point lower than that in the second quarter. The added value of the secondary industry increased by 5.2% year-on-year, higher than the overall GDP growth rate, and a significant rebound of 4.3 percentage points from the second quarter. This reflected the rapid recovery of industrial production. On the other hand, the added value of the tertiary industry increased by 3.2% year-on-year. While this was lower than the overall growth rate of GDP, it was still an increase of 3.2 percentage points from the second quarter.

In terms of the demands, in the third quarter of 2022, the contribution rates of final consumption expenditure, net exports of goods and services, and gross capital formation to economic growth were 52.4%, 27.4%, and 20.2%, respectively. Compared with the same period of the previous year, the contribution rate of consumption to economic growth in the third quarter dropped by 25.1 percentage points, indicating that consumption is still in the process of recovery. Meanwhile, the contribution rate of net exports and investment to economic growth increased by 12.7 percentage points and 12.4 percentage points respectively.

Although China's economic growth rate of 3.9% in the third quarter was slightly better than expected, the actual support of the economy in the third quarter was insufficient when viewed from itemized data.

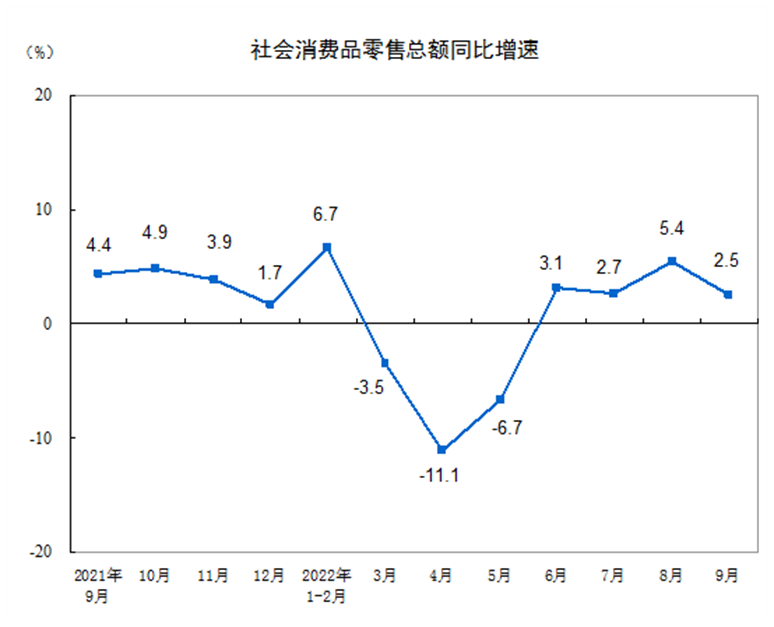

Notably, the country's domestic consumption remains sluggish. In September, the total retail sales of consumer goods increased by only 2.5% year-on-year (up 5.4% year-on-year in August), and the consumption growth from January to September this year was only 0.7% year-on-year. Obviously, three years of the impact of the COVID-19 pandemic has seriously affected consumption, the biggest pillar supporting China's economy. Not only has government consumption shrunk, but residents' consumption has also continued to slump. It should be pointed out that the downturn in consumption is closely related to the current business operations and employment conditions. Because of the closure of a large number of enterprises, the unemployment rate has been at a relatively high level. In the first three quarters, the average urban surveyed unemployment rate was 5.6%, of which the average in the third quarter was 5.4%. Due to the pandemic, the surveyed unemployment rate showed an increase in September.

Figure 2: China's Year-on-Year Growth Rate of Consumer Goods Total Retail Sales

Source: NBS

When it comes to investment, the national fixed asset investment (excluding farmers) increased by 5.9% year-on-year in the first nine months, slightly higher than the growth rate of 5.8% in the first eight months, and the overall level was basically the same. From January to September, the national real estate development investment was RMB 10355.9 billion, a year-on-year decrease of 8.0%. There is an obvious imbalance in the investment structure where private investment has continued to be sluggish this year. The growth rate of private investment in the first nine months was only 2.0% year-on-year, while the growth of state-owned enterprise investment in the same period was 10.6%. This indicates that the investment growth in the first three quarters of this year was mainly supported by the investment of state-owned enterprises, while the investment of private enterprises, which accounted for the majority of fixed investment, remained weak. A recent survey by the research team of ANBOUND also confirmed that many private enterprises are no longer making any expansionary investments for the time being, and some are still shrinking their businesses comprehensively. There is a concern that the suspension of investment by private enterprises may not be a short-term phenomenon and instead could last longer.

As for foreign trade, according to statistics from China's General Administration of Customs, in the first three quarters of this year, the country's total import and export value was RMB 31.11 trillion, an increase of 9.9% over the same period last year. Among them, exports were RMB 17.67 trillion, an increase of 13.8%. Imports were RMB 13.44 trillion, an increase of 5.2%. Meanwhile, the trade surplus was RMB 4.23 trillion, an increase of 53.7%. Calculated in the U.S. dollar, the total value of China's imports and exports in the first three quarters was USD 4.75 trillion, an increase of 8.7%. Among them, the export was USD 2.7 trillion, an increase of 12.5%. The import was USD 2.05 trillion, an increase of 4.1%. The trade surplus was USD 645.15 billion, an increase of 51.6%. It can be seen that although the growth of exports is sufficient, the growth of imports has slowed down significantly, reflecting the lack of domestic demand. However, due to the rapid expansion of net exports, the contribution to economic growth has increased as well.

In addition, the consumer price index (CPI) of the country in September was 2.8%, the highest since May 2020. The price index has been pushed up by rising pork and energy prices. Although at present it is not too high, in the context of low-income expectations and sluggish consumption, China needs to be aware of inflation. The producer price index (PPI) continued to slow down in September, a mere 0.9% year-on-year. Although the pressure on industrial production costs has been eased, it also showed that the demand for industrial production was slowing down at the same time.

Considering the current economic situation in China coupled with the impact of the COVID-19 pandemic and the poor performance of some of the above-mentioned data, we believe that there may actually be hidden worries behind the seemingly improving economic data in the third quarter. One observation window is the capital market. For the views and expectations of the economic data in the third quarter, the reaction of the capital market may be the most representative. After the third quarter economic data was released, China's A-shares fell today. The Shanghai Composite Index fell below 3000 points to 2977.56 points (down 61.37 points), or 2.02%; the Shenzhen Component Index fell 224.35 points to 10694.61 points or 2.05%. The Hang Seng Index of Hong Kong stocks fell 1030.430 points to 15180.689 points or 6.360%. At the same time, the RMB has also depreciated sharply against the USD, and the offshore exchange rate of the RMB against the USD reached 7.3 at one point.

Final analysis conclusion:

With the implementation of various policies, China's economic growth rate rebounded in the third quarter. However, the support for the economy does not appear to be solid with the presence of obvious structural defects. Most worryingly, consumption is sluggish, market confidence is seriously lacking, and private investment continues to decline. Considering these aspects, researchers at ANBOUND believe that China's economic growth rate may continue to pick up in the fourth quarter of this year, yet it remains challenging for the annual economic growth rate to exceed 4%.