With the Federal Reserve maintaining high-intensity rate hikes, the currencies of China, Japan, and South Korea, all major Asian economies, have been more or less affected to varying degrees, and are under increasing pressure of depreciation. The exchange rates of the Chinese renminbi (with the offshore exchange rate as a reference), the Japanese yen, and the South Korean won have all depreciated significantly with the appreciation of the U.S. dollar. As the three Asian countries share similar economic structures, most of them are on the main manufacturing output side. Many believe that currency devaluation will be beneficial to exports, which is conducive to long-term economic stability. Yet, if the situation of the 1997 Asian financial crisis is taken into consideration, the impact of currency devaluation on capital flows and asset values, and the "currency war" brought about by the devaluation of currencies, this may in fact bring about a sharp rise in financial risks in Asia. A few questions arose in this regard. Is a "competitive devaluation" of a currency good for the economy? Will there be another new currency crisis in Asia? Can China survive a new round of "currency war"?

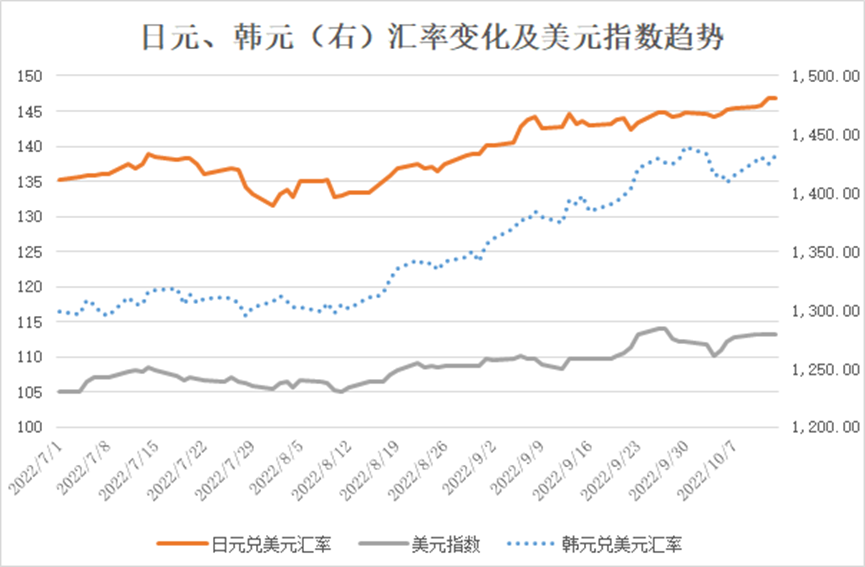

Figure 1: The Trend of JPY & KRW Exchange Rate Changes (Right) and the USD Index

Source: Investing.com. graph plotted by ANBOUND

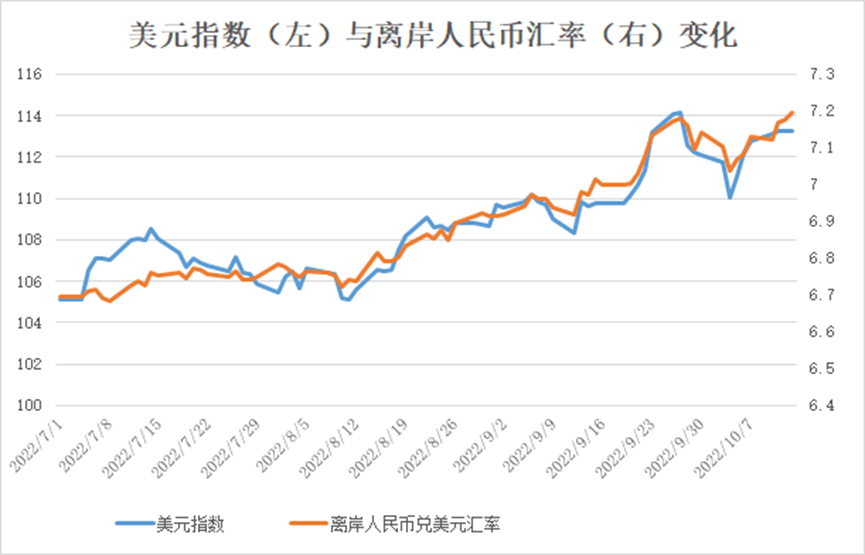

Under the circumstance that the Bank of Japan adheres to the monetary easing policy, the JPY has experienced a clear depreciation trend this year. The exchange rate of the JPY against the USD has broken the threshold position of JPY 145 to USD 1; the KRW has depreciated even more in recent months and has exceeded the level of KRW 1,400 to USD 1. Meanwhile, the offshore RMB exchange rate has passed the USD 7 boundary and is currently around USD 7.2. Japan and South Korea have experienced a turbulent situation in the capital market under the situation of rapid currency changes, where both countries have successively experienced an overall decline in stocks, bonds, and foreign exchange. This is an indication that market fluctuations are not caused by individual factors, but are more holistic. The root cause is still currency instability. The situation in China is similar. The RMB exchange rate is still closely related to the capital market. The new round of stock and bond market volatility has a direct impact on the revaluation of RMB assets due to currency depreciation.

Figure 2: USD Index (Left) and Off Shore RMB Exchange Rate Changes (Right)

Source: Investing.com. graph plotted by ANBOUND

In this sense, the view that the devaluation of the currencies of the three countries to gain an export competitive advantage seems untenable. In addition, in the context of rising global inflation and the Fed hiking interest rates, foreign trade demand will also decline across the board. In the short term, it is difficult for the manufacturing industry in the Asia-Pacific region to obtain more export opportunities through currency devaluation. Instead, the economy itself is dragged down by inflationary inputs from currency devaluation. On the one hand, Japan and South Korea have had trade deficits in goods for many months, mainly due to the increase in imports caused by the rising prices of energy, raw materials, and intermediate products. On the other hand, domestic inflation in these countries continued to rise, which further affected economic demand. Inflation in Japan reached 3% in August, a rare occasion where it surpasses the 2% policy target and a 24-year high. Meanwhile, South Korea's September CPI rose 5.6% year-on-year. Although this has dropped from a nearly 24-year high in July, it is still at a high level. Relatively speaking, although China is also under pressure, the inflation level remains below 3%, in a relatively stable state. From this point of view, it is not advisable for any country to obtain an edge over the export competition through currency devaluation.

The sharp depreciation of the currency has hit Japan and South Korea's weak macro economy, and the two governments have to use their foreign exchange reserves to rescue the market. Japan and South Korea have begun to intervene in the market, and the foreign exchange reserves of both countries have decreased by more than USD 100 billion in the past two months, reaching about USD 106.8 billion. As far as monetary policy is concerned, these two East Asian nations have adopted opposite policies to respond to the Fed’s raising interest rates. South Korea has raised interest rates for several rounds, and the policy interest rate (7-day reverse repurchase) has reached 3%. At the same time, it also has to start the way of purchasing financial assets, hoping to maintain the stability of the capital market. Japan, on the other hand, continued to adhere to easing policies and adhere to yield curve control. However, this also has a more serious impact on the Japanese stock market.

That being said, judging from the current situation, in the absence of capital flow constraints, whether a country closely follows the Fed's tightening policy or pursues the opposite easing policy, it cannot avoid the impact of international capital flows. Comparatively speaking, the situation in South Korea is more serious; though it is not exactly ideal in Japan as well. The abnormal phenomenon of “zero transaction” of Japanese government bonds has repeatedly occurred, indicating that the market is not optimistic about Japan’s adherence to the yield curve control policy.

In China, the central bank did take some countermeasures one after another, yet now it has not reversed the trend of currency depreciation. Instead, the pace of depreciation has been affected. The more favorable aspect is that China has not liberalized capital controls so that domestic shocks are limited and speculative transactions in the market are restrained. The results of the monetary policies of Japan and South Korea also show that it is feasible for China to "sacrifice" exchange rate stability in order to maintain the autonomy and independence of its domestic monetary policy.

The trend also demonstrates that it is not easy to avoid the common depreciation of currencies in major Asian economies under the dominance of the U.S. dollar. It is hence difficult for the RMB to maintain an independent situation where both circumstances both within and outside of the country are increasingly complex with weaker recovery in the country itself. The only favorable situation is that the three countries jointly bear the pressure brought by the appreciation of the dollar. This pressure has a greater impact on Japan and South Korea. However, the current situation, the stability of the respective financial systems, the level of external leverage, and the reserves of the external account, have improved significantly compared to the period of the Asian financial crisis. All three countries have adopted relatively flexible exchange rate policies, so the possibility of a recurrence of the systemic financial crisis is not significant.

Currency fluctuations reflect the stability of the economic fundamentals of the three countries. Researchers at ANBOUND have previously pointed out that the basis for the stability of the RMB exchange rate is the stability of economic fundamentals. The same is true for Japan and South Korea. Exchange rate fluctuations and economic stability are in fact, interacting with each other. In this case, China is still in a relatively favorable position among the three countries by the virtue of its market capacity and capital account constraints. This, as things turn out, is the basic condition for winning the "currency war". Of course, under the circumstances that the economic, trade, and financial fields are closely linked, the occurrence of a "currency crisis" in neighboring countries is never good news for China. When this happens, the country itself needs to bear more pressure, the exchange rate will fluctuate more, and it will be more difficult to manage the complex situation.

Final analysis conclusion:

Japan, South Korea, and China all experience currency depreciation to varying degrees under the impact of the Fed's tightening policy. For these countries, the benefits of currency devaluation are currently far less than the damage it causes. Therefore, maintaining exchange rate stability is necessary for the respective and common interests of all of them. With its current economic stability and market size, China still has an advantage in coping with dollar shocks.