In the financial statistics for August that were announced by the People's Bank of China (PBoC) on September 9, the increase in social financing in August was RMB 2.43 trillion, being RMB 557.1 billion less than the same period last year, according to the preliminary statistics. The Chinese currency loans increased by RMB 1.25 trillion in August, a year-on-year increase of RMB 39 billion. At the end of August, the balance of broad money (M2) was RMB 259.51 trillion, a year-on-year increase of 12.2%, up 0.2 percentage points from the end of July. On the other hand, narrow money (M1) increased by 6.1% year-on-year, down from 6.7% at the end of July, which is also a decrease of 0.6 percentage points. The increase of the social financing scale in August was RMB 2.43 trillion, a significant rebound from the previous value of RMB 756.1 billion, yet this was also RMB 557.1 billion less than the same period of the previous year. The stock of social financing scale at the end of August was RMB 337.21 trillion, up 10.5% year-on-year, though it is a drop of 0.2 percentage points from 10.7% at the end of July.

Looking at the statistics for the month of August, although the scale of monetary growth continued to rise, and at the same time there was the increase in the scale of credit promoted the hike of new social financing, the decline in the overall growth rate of social financing indicated that the comprehensive demand remained weak. Researchers at ANBOUND are of the opinion that, China is in a financial environment of "loose money" and "tight credit". The country, as things stand, is promoting the improvement of effective demands. In its macro policies, demands are taking an increasingly larger proportion.

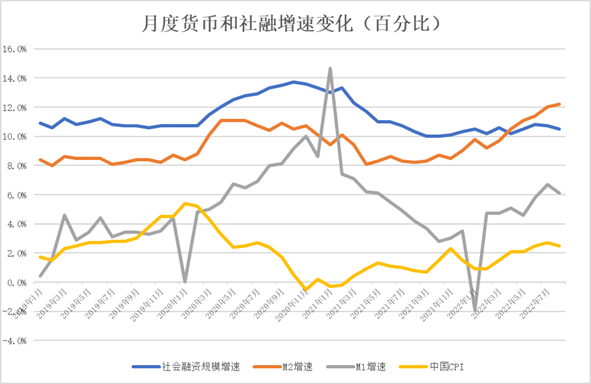

Figure: Monthly Monetary and Social Financing Growth Change (%)

Source: PBoC, NBS

Chart plotted by ANBOUND

Driven by a series of easing policies such as RRR cuts and interest rate reductions in the previous period, since March, the growth rate of M2 has maintained a continuous growth trend. The general monetary environment in China, as it appears, still displays a "loose" trend. However, this "loose money" has not been able to promote the recovery of finance. The growth rate of the M1 slowed down significantly in August, signifying that the daily operations of businesses are still plagued by various factors and have yet to fully recover from the impact of the COVID-19 outbreaks. Correspondingly, inflation in China slowed down in August, and both CPI and PPI fell. In the case of rising food prices, including pork prices, CPI growth was still lower than that in July, though there was a factor of decline in energy prices. The core CPI increased by 0.8% year-on-year, unchanged from the previous value, and the core inflation remained sluggish. At the same time, the continuous decline of PPI poses the fear that China might return to the pattern of overproduction. All these, in fact, reflect that the demands in China have not rebounded strongly due to the influence of the pandemic, as well as because of other internal and external factors. Under the continuous impact of COVID-19, the market is expected to face difficulty to recover effectively. This, in turn, contributes to the slow recovery of the entire economic demands.

The scale of RMB credit, which reflects major financial needs, showed a downward trend amid the change in expectations. In terms of scale, the increase in the Chinese currency loans in August recovered significantly from that in July. In August, the loans increased by RMB 1.25 trillion, up RMB 39 billion year-on-year. Based on sectors, household loans increased by RMB 458 billion, of which short-term loans increased by RMB 192.2 billion, and medium and long-term loans increased by RMB 265.8 billion.

Enterprise (institutional) loans increased by RMB 875 billion, of which there is a drop of RMB 12.1 billion in short-term loans, while medium and long-term loans increased by RMB 735.3 billion, bill financing increased by RMB 159.1 billion; while loans to non-banking financial institutions decreased by RMB 42.5 billion. The increase in medium and long-term loans to enterprises was mainly due to the obvious increase in the investment demand. Some analysts pointed out that the rapid implementation of quasi-fiscal tools has shown a strong role in boosting the demand for infrastructure supporting financing. At the same time, it is worth noting that the structure of new loans in August was differentiated, showing stronger demands among enterprises yet weaker for households.

In August, medium and long-term loans to households still increased significantly year-on-year, reflecting the shrinking demands caused by the downturn in the real estate market. However, the increase in the scale of RMB loans was insufficient to promote the growth of the stock. The balance of RMB loans at the end of August was RMB 208.28 trillion, a year-on-year increase of 10.9%. This is an indication that demand growth remains sluggish. The scale of credit has only rebounded several times under the stimulus of policy, while the growth performance still lacks sustainability.

The increase in the social financing scale in August 2022 was RMB 2.43 trillion. While there was a significant recovery from July, it was still RMB 557.1 billion lower than the same period last year, excluding seasonal factors. Among them, RMB loans issued to the real economy increased by RMB 1.33 trillion, a year-on-year increase of RMB 63.1 billion. Foreign currency loans issued to the real economy decreased by RMB 82.6 billion, a year-on-year drop of RMB 117.3 billion. Entrusted loans rose by RMB 175.5 billion, a year-on-year increase of RMB 157.8 billion. Trust loans decreased by RMB 47.2 billion; a year-on-year drop of RMB 89 billion. Undiscounted bank acceptance bills increased by RMB 348.5 billion, a year-on-year increase of RMB 335.8 billion. Corporate bond net financing was RMB 114.8 billion, a year-on-year drop of RMB 350.1 billion. Net financing of government bonds was RMB 304.5 billion, a year-on-year decrease of RMB 669.3 billion. Stock financing of non-financial enterprises within the country was RMB 125.1 billion, a year-on-year decrease of RMB 22.7 billion. From January to August, the cumulative increase in the social financing scale was RMB 24.17 trillion, this figure is RMB 2.31 trillion more than the same period of the previous year. The increase in social financing is closely related to direct government financing. It appears that the advance issuance of local government bonds has contributed to the decline in social financing in August this year. With little change in credit, the scale of bill financing has grown significantly, indicating that the overall credit environment has not improved dramatically.

Comparing the growth rate of social financing stock with the growth rate of M2, since the crossover in April, the gap has gradually widened, which means that the overall credit environment is still "tight" compared with monetary expansion. Researchers at ANBOUND believe that, on the one hand, financial institutions are still cautious about the future profits of enterprises and have not improved their credit expectations with the loosening of monetary policy. On the other hand, it also shows that in the case of a weak economy, a large number of market entities are actually in an extremely weak state, thereby lack of effective financing needs, resulting in repeated declines in the scale of new credit.

Therefore, although the overall financing demand has rebounded from July, it is far lower than the improvement in the money supply. It is true that the market confidence, as a whole, has recovered, but it is still weak under multiple uncertain factors such as the COVID-19 outbreaks. The sustainability of the market for future economic growth, therefore, remains challenging.

For ANBOUND's researchers, the weak overall demand means that the demand for monetary policy easing has weakened, while the credit of market players has also become obviously weaker than in the early stage of the pandemic in 2020. Instead, the money supply is greater than the effective financial demand. Hence, the main contradiction now is not entirely on the supply side, but more on the demand side brought about by changes in the economic environment. In the case of slowing demand, the focus of China's macro policy needs to be adjusted, from promoting an easing environment and easing money supply to expanding effective demand, so as to improve and expand market financing needs and maintain the continuity of credit scale growth.

Final analysis conclusion:

Monetary and social financing statistics indicate that in August, the performance in China appears to have recovered. However, the gap between the growth rate of social financing and monetary was widening, reflecting the country's financial environment of "loose money" and "tight credit". The worsening economic environment and unstable market expectations have resulted in weak effective demand, which are the main reasons for the fluctuation of credit scale and the slowdown in economic growth. In order to achieve the goal of stable growth, the Chinese policymakers will need to emphasize more on promoting the improvement of effective demand in the country's future macro policies.