As the exchange rate of RMB against the USD continued to depreciate, the People's Bank of China (PBoC) has made corresponding policy adjustments. On the afternoon of September 5, the central bank announced that in order to improve the ability of financial institutions to use foreign exchange funds, it decided to reduce the foreign exchange reserve ratio of financial institutions by 2 percentage points from September 15, 2022, that is, down from the current 8% to 6%. This is the second time this year that the PBoC has lowered the foreign exchange reserve ratio. On April 25, the Chinese central bank announced that from May 15, the foreign exchange reserve ratio of financial institutions will be lowered by 1 percentage point to 8%. The reduction of the foreign exchange reserve ratio this time has reached 2 percentage points, which is stronger than the adjustment in April, and its policy signal is also clearer.

In the opinion of researchers at ANBOUND, the purpose of the foreign exchange reserve ratio adjustment is not to reverse the general trend of RMB depreciation, but to prevent the process of RMB depreciation from "derailing".

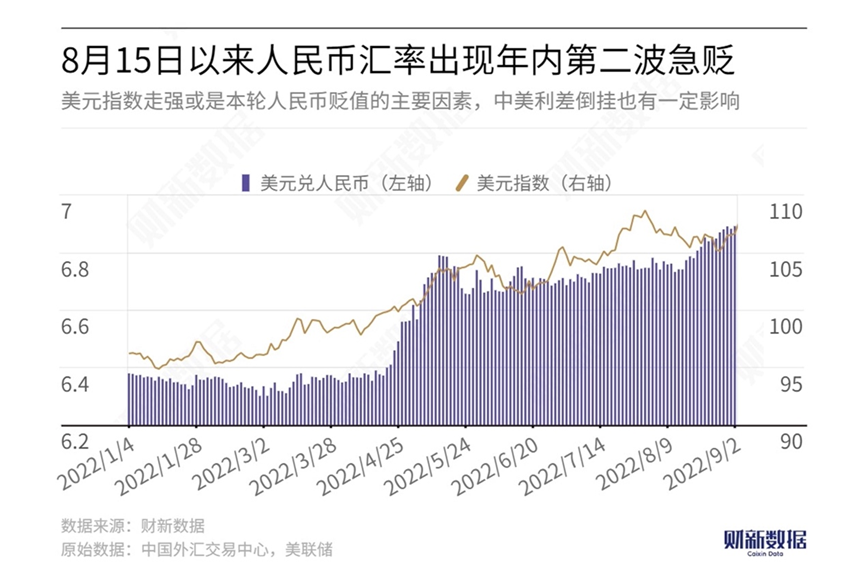

Figure: Depreciation of the RMB since August 15

Source: Caixin Data

Since mid-August, the exchange rate of the RMB against the USD has continued to depreciate. At 16:30 on September 5, the onshore RMB closed at 6.9366 against the USD, down 338 basis points from the previous trading day and hitting a new low since August 2020. Since the PBoC cut its policy rate on August 15, the Chinese currency has lost 2,017 basis points, or 2.9 percent, against the dollar. The central parity of the RMB against the USD fell from 6.7413 to 6.8998 on September 5, down 1,585 basis points, or 2.35%. According to the latest data available from the PBoC, as of the end of July, the balance of foreign currency deposits was USD 953.7 billion. The reduction of the foreign exchange reserve ratio of financial institutions by 2 percentage points, according to media estimates, will release about USD 19 billion of foreign exchange liquidity. As the RMB exchange rate against the USD continues to depreciate and is only one step away from reaching RMB 7 to USD 1 threshold, the central bank adjusts the foreign exchange reserve ratio to release foreign exchange liquidity for commercial banks and increase the supply of the dollar foreign exchange. This will alleviate the pressure on the continued decline of the RMB exchange rate to a certain extent. Market data shows that after the PBoC's foreign exchange reserve ratio cut, the onshore and offshore RMB exchange rates have adjusted to varying degrees.

However, it should be pointed out that the foreign exchange rate reduction policy is still insufficient to alter the general trend of the RMB exchange rate continuing to decline. For this round of RMB exchange rate depreciation, there is not only a lack of market confidence caused by the slowdown of China's economy but also by external pressure from the Federal Reserve's expectation of raising interest rates. Under the influence of various internal and external complex factors, researchers at ANBOUND believe that with the continuous appreciation of the USD and the accelerated pace of monetary tightening by the Fed, the RMB exchange rate still has a tendency to depreciate in stages. Although the PBoC has taken some measures to prevent the depreciation of the RMB exchange rate from getting out of control, it will not change the phased trend of RMB depreciation under the widening differences in the monetary policies of China and other countries.

The question is, why then, should the PBoC intervene? In fact, under the general trend of RMB depreciation, market trend changes are crucial for the RMB exchange rate too. Under such circumstances, the Chinese central bank has launched its policy from time to time to avoid the formation of a unilateral market with unanimous market expectations, as well as to prevent the risk of "derailment" as mentioned by ANBOUND. In the short term, the PBoC has initiated some hedging policies, so that the RMB still maintains a two-way fluctuation in form. As Liu Guoqiang, the PBoC deputy governor previously noted, the Chinese currency should fluctuate in two directions, and there will be no "unilateral market" when there are two-direction fluctuations. "A reasonably balanced and generally stable renminbi is what we are happy to see, and we have the capacity to support it. I don't think there will be any accidents, nor will there be allowed to be any accidents," Liu said. Therefore, the central bank's reduction in foreign exchange reserve is to maintain the "two-direction fluctuations" of the Chinese currency and avoid the panic of market speculation that might exacerbate the devaluation of the RMB.

After a period of pressure release, the central bank's intention is to maintain an "orderly" devaluation of the RMB to avoid vicious depreciation. From the perspective of the PBoC's policy reserves and its control of the overall RMB and foreign exchange liquidity, the central bank does indeed have the ability to effectively control the fluctuation of the exchange rate. Liu also emphasized that China's foreign exchange market is currently operating normally, and so are the cross-border capital flows. Although the spillover effect of U.S. monetary policy can be seen, the impact remains controllable. That being said, this does not mean that the PBoC can reverse the trend. With the monetary policy remaining stable and the interest rates not being hiked easily, the devaluation of the RMB exchange rate is also a compromise that has to be made to release the pressure of unbalanced internal and external monetary policies.

As for whether the exchange rate of the RMB against the USD will reach the RMB 7 to USD 1 threshold. Researchers at ANBOUND believe that reaching the specific point is not important for the PBoC's policy goals, nor for the Chinese economy. Even if the RMB exchange rate reaches the said threshold in the future, it is something that is expected and in fact, normal. During the outbreaks of COVID-19, the exchange rate of RMB against the USD once reached the level of 7.2, and there was no exchange rate risk being spread. The root of this lies in the stability and resilience of the Chinese economy. ANBOUND has previously pointed out that, on the one hand, this round of RMB depreciation is dominated by the strong USD brought about by the Fed's aggressive interest rate hike policy whose effects can be felt throughout the world, and the RMB is no exception. On the other hand, China's economy is showing signs of "bottoming out" under the continuation of the pandemic. While it will take time to recover, the country still shows stable resilience as a whole. The stability of China's economy and market actually makes the room for its currency to have a limit in its depreciation. In the case of continuous release of pressure, the pace of RMB depreciation may further slow down in the future.

Final analysis conclusion:

The PBoC's reduction of the foreign exchange deposit reserve ratio is to maintain the two-sided market trend of the Chinese currency and avoid the formation of unanimous expectations that might cause the depreciation of the RMB exchange rate to "derail". This move, however, is not to reverse the general trend of RMB depreciation. The basis for the steadiness of the RMB is still the stability of China's economy.