Wang Dongtang, a senior officer at China's Ministry of Commerce, has recently stated that since 2012, the country's import and export of service trade has maintained a rapid growth momentum, with an average annual growth rate of 6.1%, 3.1 percentage points higher than the global growth rate. China's service trade in global ranking has risen from third place to second, and last year it ranked second in the world for eight consecutive years.

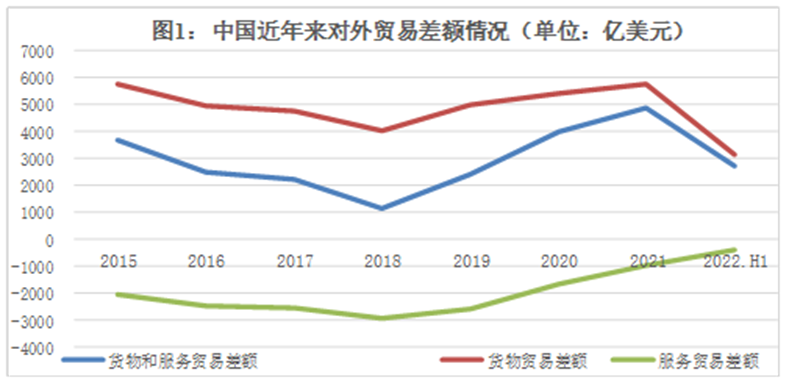

The Ministry of Commerce also expressed that since 2018, the country's service trade deficit has shown a gradual decline. This is especially true that, since the outbreak of the COVID-19 pandemic, there is a sharp drop in travel imports and exports. In addition, the increase in exports of traditional services and emerging services are also the main factors behind the decline in the service trade deficit. With the development of China's economy and the transformation of its economic structure, similar to commodity trade, service trade as an integral part of foreign trade, has indeed shown a trend of rapid growth. Regarding the prospects for the development of China's service trade in the future, relevant authorities of the State Administration of Foreign Exchange (SAFE) said that the development pattern of the country's service trade will continue to upgrade and evolve. With the continuous improvement of service export competitiveness, service trade revenue will continue to grow.

Under the overall optimistic trend, researchers at ANBOUND are of the opinion that despite the strong potential of China's service trade, its development still faces multiple challenges and uncertainties. Under unstable factors such as the continued outbreaks of COVID-19 and increasing geopolitical risks, it would be crucial for the country to maintain a balance between stabilizing growth and risk prevention. In particular, there should not be excessive optimism about the sharp drop in the trade deficit in services due to the pandemic. Furthermore, China also needs to improve the quality and added value of service trade, so as to enhance its competitiveness in the service industry. Realizing all these, and achieving the goal of transforming "Made in China" into "China's Service" will be a long-term challenge for the country's foreign trade.

Figure: China's Trade Deficit in Recent Years (unit: hundred million dollar)

Source: SAFE, Chart plotted by ANBOUND

Unlike commodity trade, which has always been in surplus, China has maintained a deficit in service trade for many years. This is not only detrimental to the stability of its foreign trade structure but also has a negative effect on its economic growth. It should be pointed out that the deficit in trade in services has fallen sharply since the pandemic. One of the main factors is the decline in travel imports caused by the deficit, and this decline is mainly due to the travel restrictions imposed by various countries, which limit the activities of Chinese citizens in traveling and studying abroad. When such restrictions are gradually lifted in the future, this aspect may rebound, leading to a situation where the deficit widens. Therefore, China needs to see the short-term deficit change more rationally, without being overly optimistic about the long-term one.

From another perspective, the large number of imports of travel services indicates that there is a strong domestic demand for related tourism, education, and medical services. Establishing effective supply in related fields and realizing "import substitution" for travel service demand not only plays an important role in reversing the deficit in service trade, but is also critical in building a large domestic market. It is then, of great significance to realize the transformation and upgrading of the country's economic structure. Since China's reform and opening up, it has participated in the process of globalization by developing its manufacturing industry, earning its status as the "world's factory". To this day, Chinese society remains strongly "production-oriented". The development of the service industry, consumption, and service trade is, therefore, its shortcomings. However, in the future, China's economy will develop and upgrade, transforming into a consumption-based society. The development of the service industry and service trade will become the general trend. However, in contrast with the manufacturing industry, the service industry has higher requirements for human resources and is a typical labor-intensive industry. The improvement of tourism, education, and medical service capabilities not only requires a large number of high-quality labor but also long-term accumulation in science and technology, culture, and other aspects. In addition, it needs a stable and healthy market environment. In this regard, there are still many fundamental deficiencies in China. Resolving these issues may require longer time and resource investment, as well as persistent policy guidance and support.

In the service industry, a major deficit aspect is the difference in intellectual property royalties. The current related deficit has not only not been reduced, but continues to expand instead. Although China's intellectual property exports are also growing rapidly, there is still a big gap compared with a large number of imports. This certainly does reflect the introduction and improvement of its science and technology, as well as the improvement of intellectual property protection. Similarly, this also reflects the considerable gap between China and developed countries in terms of technological innovation and corporate brand building. In order to improve the scientific and technological strength and the overall capability of enterprises, the deficit in this aspect is not exactly a bad thing. That being said, it would be crucial for China to promote the digestion of imported technologies while further increasing the pace of opening up, so as to drive the continuous progress of its own domestic scientific and technological development. This, in turn, helps to achieve a balance of related trade. In addition, although many Chinese enterprises can rank among the top global enterprises in terms of scale, very few of them have real influence in the international market, and neither do they become global brands. It is then necessary to promote such enterprises to establish China's own branding. At the same time, it should be noted that brand building is also not something that can be achieved overnight, and requires these enterprises to continuously enhance their skills and improve the relevant business environment.

At the same time, it should be noted that in insurance and other fields, China also maintains a considerable deficit, which also reflects the gap between its financial and insurance services with those of other developed countries. These gaps need to be treated correctly by further promoting the opening of related fields, attracting related companies to enter the Chinese market, and improving the capabilities of domestic related industries while achieving "localization". The Ministry of Commerce also mentioned that trade in services has played an important role in optimizing the structure, promoting employment, and stimulating consumption. It is also noticeable that the problem of unbalanced and insufficient development of China's service industry is still prominent, especially the development level of modern service industries with high added value such as finance and technology. Moreover, there is still a certain gap compared with developed economies. Therefore, to achieve a balance in service trade, it is more about the ability of related industries to make up for the shortcomings as soon as possible.

In areas like computing, information services, and other commercial services including scientific research and consulting, China has the advantages and can maintain a surplus. The export of services in these fields has made major contributions to reducing its trade deficit in services. This also acts as a reflection of China's relevant competitiveness, including its internet and telecommunications companies. However, these areas currently need to consider the challenges brought about by the deterioration of the external trade environment due to geopolitical competition. Furthermore, they also need to face competition from other emerging market countries with more cost advantages. In particular, the U.S. continues to strengthen its sanctions against Chinese internet and telecommunications companies, and related trade barriers are also expected to increase. For such reasons, it is even more necessary for China to make relevant preparations. This includes hastening negotiations on trade in services with other countries, and actively participating in the formulation and coordination of international rules on digital trade, creating conditions and guarantees for expanding and stabilizing overseas markets.

Final analysis conclusion:

China's service trade has shown a strong momentum of development in recent years, yet it remains in a state of trade deficit for a long time. This is certainly not conducive to the stability of foreign trade and the domestic economic growth of the country. Improving the structure of service trade is not only about reducing the deficit, but also the need to further open up and introduce technology and management models. In addition, China should also overcome shortcomings in the development of the service industry, and focus on enhancing the competitiveness of its domestic tertiary industry. This is so that it will be able to transit from a "production-oriented" society to a "consumption-based" one, which opens up new growth areas for its economy.