On July 15, China’s National Bureau of Statistics (NBS) announced the economic data of the country for the first half of the year, which had a certain impact on the market. Most of the market's attention is centered on the significant slowdown in China's economic growth, with a year-on-year growth of 2.5% in the first half of the year. In the second quarter, the year-on-year growth was only 0.4%, barely achieving the goal of maintaining positive growth proposed by Premier Li Keqiang in late May.

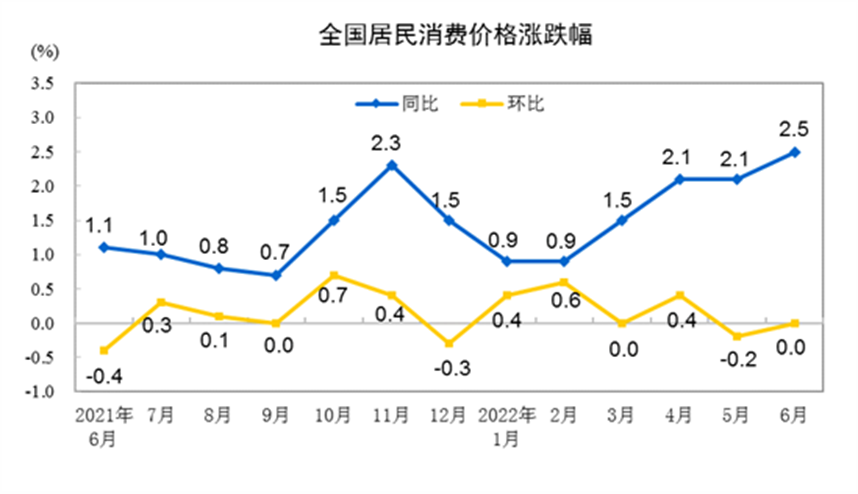

China's inflation rate in the first half of the year does not seem to be eye-catching. During this period, the national consumer price index (CPI), a key indicator used to measure the inflation rate, rose by 1.7%. The rise was 1.1% in the first quarter and 2.3% in the second quarter. If considering the index on monthly basis, the CPI was lower than the previous year but higher than the same period last year, with a moderate upward trend. In January and February, affected by factors such as the rise in international commodity prices and the Spring Festival, the CPI rose by 0.9% year-on-year. In March and April, with the outbreaks of COVID-19 and the continued high international energy prices, the CPI rose year-on-year, expanding to 2.1% month by month. In May and June, as the measures against COVID-19 stabilized, logistics gradually improved. However, due to the low base in the same period last year, the year-on-year CPI growth rate was still 2.1% in May, and grew to 2.5 in June %. Such inflation is unremarkable and still within the safe distance from the 2022 full-year inflation target of 3%.

Figure: China’s National Consumer Price Growth

Source: National Bureau of Statistics

On the other hand, other countries in the world, especially in the West such as the United States and many European countries, are under the pressure of the highest inflation in 40 years. The U.S. CPI in June increased by 9.1% year-on-year, higher than the previous value (8.6%) and market expectations, hitting a new high since November 1981. Among them, energy prices rose 41.6% year-on-year, the highest since April 1980. Food prices rose 10.4% year-on-year, the highest since February 1981. Affected by the situation in Ukraine, energy and food prices in the eurozone continued to soar, and the inflation rate in June reached a record high of 8.6% on an annual basis. Energy prices in the eurozone rose by 41.9% year-on-year in June, being the main reason for the hike in inflation for the month. As for the inflation rate of the major EU economies in June, it was 8.2% in Germany, 6.5% in France, 8.5% in Italy, and 10% in Spain. All these were at high levels. In addition, the inflation rate of the three Baltic countries rose as high as 20%.

Due to the increase in energy prices and food prices brought about by the war in Ukraine, the inflation rate in the United States and European countries rose to a unresolvedly high. China too is highly dependent on foreign energy and is also affected by rising energy prices, but why is its inflation rate so different from that of the United States and Europe?

Indeed, China's inflation rate has formed a huge contrast with the West over the same period. Its inflation rate of around 2% is surprisingly good compared to that of the West. In a high inflation global environment, China's low inflation stands out among the nations. While this might look optimistic, there are still many internal problems and risks that call for the country’s attention.

ANBOUND’s founder Chan Kung believes that inflation and economic growth are some of the most difficult issues to comprehend, yet they are also the easiest indicators to be misinterpreted. As these issues are part of a larger subject that can encompass variegated points of concern, the subject matter can be constructed and understood in multiple ways. That being said, this larger subject does in fact possess its own scales and standards, and in reality, it can only selectively include certain issues. Whether it is the inflation rate or the economic growth rate, these are in actuality the larger picture resulting from the amalgamation of various elements.

China's inflation rate in June was 2.5%. While this figure is not high, it indicates the existence of multiple issues. Chan Kung believes that the inflation rate is actually linked to the economic growth rate. Such an understanding allows a more objective interpretation of the data. The inflation rate in China was 1.7% in the first half of the year and 2.5% in June. Correspondingly, its economic growth rate in the first half of the year was 2.5%, a considerably low rate and a result of the current economic situation. This signifies that at present, economic activities are at a seriously low ebb, as they are unable to be carried out normally and are in a state of being frozen. When this happens, economic transactions cannot take place. Therefore, the economic growth rate will appear as low as 2.5%.

Under such circumstances, the price factor will naturally not be reflected as there are no transactions. For any transaction, when there is a price and when the price is negotiated, this would mean that the transaction activity is an economic activity. Therefore, we emphasize that the economic growth rate should be linked to the inflation rate. This makes understanding and interpreting the current inflation rate clearer. Chan Kung is of the opinion that China's low inflation rate is mainly due to the relatively low economic growth rate. In a real-world setting, there are more potential price hikes. For example, China's refined oil prices rose 10 times this year and fell twice. With this, the fuel surcharge of air tickets in the country rose for 5 consecutive months from February this year to the current time, and the price has increased by 10 times. A flight from Zhengzhou to Lanzhou on July 12 cost only RMB 237, but the fuel surcharge has risen to RMB 250, even higher than the ticket price.

Is the phenomenon of such a sharp rise in prices fully reflected in the inflation indicator? The answer is “no” according to Chan Kung. Therefore, the current low inflation rate in China may only be a temporary phenomenon. If the country's economic activities continue to be frozen for various reasons, then its inflation rate may be further distorted. However, sooner or later, China's inflation rate will increase dramatically, followed by explosive growth.

Final analysis conclusion:

If inflation and economic growth are linked, what is reflected will be consistent with the data, and shows the real inflation rate in China.