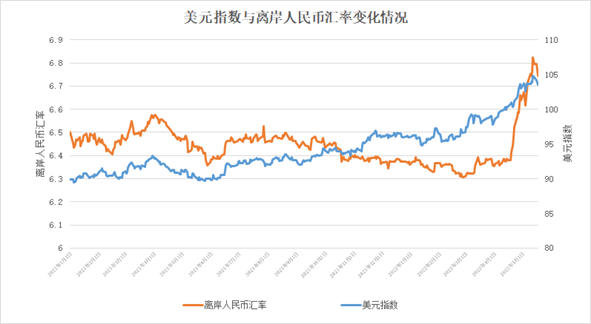

Figure: Changes in the U.S. dollar index and offshore RMB exchange rate

Source: Investing.com, plotted by ANBOUND.

The central parity rate of USD/RMB in the inter-bank foreign exchange market was 6.7854 on May 17, up 17 basis points from the previous value, according to the China Foreign Exchange Trade System. Meanwhile, the U.S. dollar index fell back below 104, down 0.32% during the day to 103.88. The offshore RMB exchange rate recovered two important levels in a row on May 17, while the onshore RMB exchange rate once recovered the 6.76 mark. As of 16:30 Beijing time, the onshore and offshore RMB exchange rates were at 6.7557 and 6.7609 against the USD, up 304 and 364 basis points respectively from the previous close. Since April 19, the RMB has been falling against the USD, and even depreciated to the 6.8 mark on May 13, hitting a new low since October 2020. The RMB exchange rate has recently shown a stabilizing trend amidst the fluctuation of the U.S. dollar index. This actually suggests a further strengthening of the correlation between the U.S. dollar index and the RMB exchange rate.

Wang Chunying, deputy administrator of the State Administration of Foreign Exchange (SAFE), said the RMB exchange rate has depreciated a little against the USD recently, but it is still relatively stable compared with other major currencies. In terms of multilateral exchange rates, the RMB remains basically stable against a basket of currencies. Wang said that to observe the trend of the RMB exchange rate, it is necessary to see not only its short-term two-way fluctuations, but also its long-term stable fundamentals. Whether the RMB exchange rate appreciates or depreciates in phases in recent years, it is reflected in more normalized two-way fluctuations. The overall trend remains basically stable at a reasonable equilibrium level.

As for the future trend of the RMB, many market participants believe that the trend of the RMB exchange rate will still face a variety of uncertainties. Researchers at ANBOUND believe that the RMB exchange rate is still affected by multiple internal and external factors, mainly the USD. Despite the current recovery of the RMB exchange rate, the monetary policies of China and the U.S. are still influencing each other, and the external factors will become more complicated with the changes in the monetary policies of the European Central Bank and the Bank of Japan. Under the circumstance of intensified geopolitical currency game and obvious divergence trend, the RMB exchange rate is still under great pressure. Keeping the exchange rate stable and flexible remains important for China's economic stability.

Chan Kung, founder of ANBOUND, believes that the U.S. has started its plan to raise interest rates to ease inflation, thus driving the USD stronger, while the use of exchange rate tools is conducive to the U.S. to ease inflationary pressure, which will put pressure on the RMB exchange rate and may drive capital outflows from China. In other words, due to the dominant position of the Federal Reserve in global monetary policy, the trend of a stronger dollar will continue in the future as the U.S. gradually implements interest rate hikes and tapering. Brian Deese, director of the White House National Economic Council, said recently that the strength of the dollar reflects the strength of the U.S. economy. This shows that the U.S. government is happy to see a stronger dollar. Compared to the EUR and the JPY, China, as the second-largest economy, has very close trade and investment ties with the U.S. Therefore, the RMB is more affected by the changes in the USD, and its exchange rate will bear the brunt of the impact under the trend of dollar appreciation. In the case of increasing differences between the monetary policies of China and the United States, the RMB still faces the pressure of periodic depreciation.

In terms of the euro, although the European Central Bank hopes to raise interest rates and start tapering in July to push up the EUR and slow down the trend of the continued appreciation of the dollar, it is difficult for the EUR to perform strongly under the situation that the conflict between Russia and Ukraine is prolonged, with the European Union and the eurozone economy being affected by energy issues and wars. At the same time, in the case of Japan, the third-largest economy, the yen has seen a persistent depreciation under the Bank of Japan's continued push for monetary easing, with the JPY depreciating even more than the RMB. Such competitive depreciation widens the divergence among major international currencies and will further drag down the stability of the RMB.

Although the current short-term trend of "two-way fluctuations" in the RMB is conducive to avoiding currency arbitrage and slowing down the depreciation of the RMB, the long-term external factors of the RMB exchange rate will be more complicated under the circumstance of increasing geopolitical risks, and it is difficult to see a sharp rebound what happened in 2021.

Internally, researchers at ANBOUND have repeatedly emphasized on maintaining the stability of the RMB exchange rate and economic fundamentals. It can be said that the factors causing the recent depreciation of the RMB exchange rate have a great deal to do with the increase of downward pressure on China's economy and the contraction of demand under the pandemic, which reflects the change of expectations on RMB assets and economic growth. As the pandemic prevention and control efforts are taking effect and the domestic economy is stabilizing due to the resumption of work and production, the RMB exchange rate needs to achieve a new level of equilibrium, which still needs the support of economic stability.

ANBOUND has previously pointed out that the biggest risk of RMB exchange rate fluctuation comes from capital outflow, which not only affects China's financial stability, but also poses a threat to China's economy. This risk actually comes not from the outflow of foreign financial capital, but from the panic outflow of domestic capital. The response to RMB depreciation should therefore be prioritized over stronger domestic capital controls. This means that the RMB exchange rate mechanism still needs to adhere to the "two-way fluctuation", so as to avoid short-term fluctuation exacerbating market panic and forming a vicious circle.

The "impossible trinity" of the Mundell-Fleming Model states that it is impossible for a state to have fixed exchange rate (regime), sovereign monetary policy, and free capital flow at the same time. Under the condition of adhering to sovereign monetary policy and strengthening capital control, the fluctuation of the RMB exchange rate is an inevitable trend. Therefore, as far as the RMB exchange rate policy is concerned, the stability of the RMB exchange rate does not mean that the exchange rate is fixed at a certain level, but rather that it needs to "adapt to the situation" to maintain stability and order in the process of exchange rate changes, and to establish a new equilibrium amidst the changes in the monetary policies of China and the U.S. by guiding the RMB to depreciate gradually. The recent depreciation of the RMB exchange rate has in fact already released some pressure. Although it has brought volatility to the capital market, it has also released space for the sovereign monetary policy and brought opportunities for export recovery. Under such circumstances, monetary policy needs to focus more on achieving economic stability and building a firm "momentum" for the stability of the RMB exchange rate.

Final analysis conclusion:

The RMB exchange rate has become more volatile. Although there is a gradual recovery at present, it is still more of a "two-way fluctuation". In the context of increased geopolitical risks, the intensified monetary policy game between China and the U.S., and increased downward pressure on the domestic economy, the RMB exchange rate is still under pressure. Under such circumstances, the exchange rate policy needs to adapt to the situation and transition the exchange rate to a new equilibrium point in an orderly and stable manner.