On December 15, China's National Bureau of Statistic today released certain economic data for November. All in all, after the Central Economic Work Conference was held, analyzing China's economy from November's economic data does not offer much value in forming a judgment on the country's economic trends. First, because the data has lagged behind, and the data for the last two months has little impact on the overall economy; second, the Central Economic Work Conference has made a judgment on the situation and determined the policy tone for next year, in addition to that various departments of the State Council are already deploying next year's work accordingly. That said, we can still observe the current situation, problems, and possible risks of China's economy from the economic data in November. Overall, a number of economic data in November showed that China's economy is slowing further, and downward pressure continues to increase, dragging down the strength of China's post-pandemic recovery this year. In terms of growth rate, the average annual GDP growth rate in the first, second and third quarters of this year was 5%, 5.5% and 4.9% respectively, and the economic growth rate dropped significantly in the third quarter, indicating that there is obvious downward pressure on the economy.

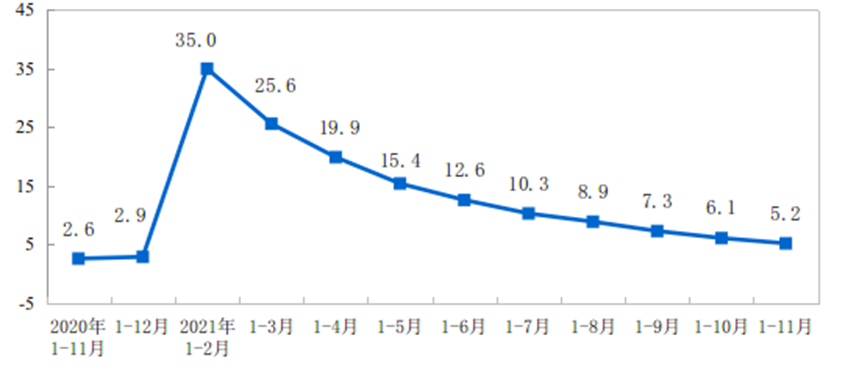

Judging from the itemized data, in terms of investment, from January to November, the country's fixed asset investment (excluding farmers) was RMB 49,408.2 billion, an increase of 5.2% year-on-year (down 0.9 percentage points from 6.1% from January to October), rising 7.9% from January to November 2019, which is an average increase of 3.9% in the two years. Private fixed asset investment was RMB 28,102.7 billion, an increase of 7.7% year-on-year. In terms of real estate investment, from January to November, the country invested RMB 13,731.4 billion in real estate development, an increase of 6.0% year-on-year, down 1.2 percentage points from 7.2% from January to October. Previously, according to data released by China's central bank, at the end of November 2021, the balance of personal housing loans was RMB 38.1 trillion, an increase of RMB 401.3 billion in the month, and the real estate loans of banking financial institutions increased by more than RMB 200 billion year-on-year. Obviously, the real estate lending data that began to moderate did not reverse the decline in real estate investment.

Figure 1: Year-on-year growth rate of fixed asset investment (excluding farmers) (%)

Source: National Bureau of Statistics Website

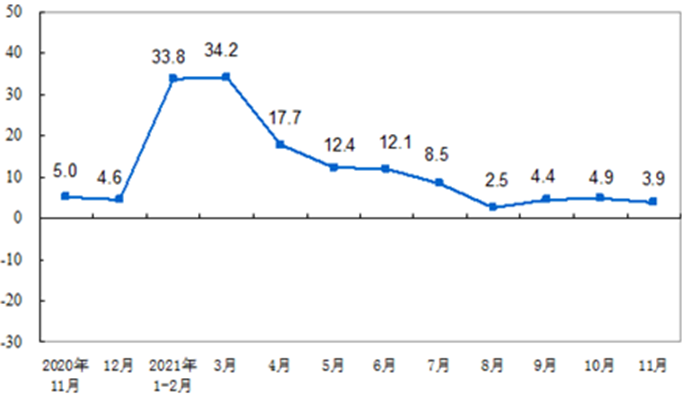

Looking at consumption, in November, the total retail sales of consumer goods totaled RMB 4,104.3 billion, an increase of 3.9% year-on-year (4.9% in October); which is also a rise of 9.0% over November 2019, and the two-year average growth rate was 4.4%. Among them, the retail sales of consumer goods other than automobiles totaled RMB 3,726.6 billion, an increase of 5.4%. Excluding price factors, the total retail sales of consumer goods increase by 0.5% year-on-year in November. From January to November, the total retail sales of consumer goods totaled RMB 39,955.4 billion, an increase of 13.7% year-on-year, up 8.2% from January to November 2019. The retail sales of consumer goods other than automobiles totaled RMB 36,033.9 billion, an increase of 14.0%. From January to November, national online retail sales totaled RMB 11,874.9 billion, an increase of 15.4% year-on-year. To further break down, online retail sales of physical goods were RMB 9,805.6 billion, an increase of 13.2%, accounting for 24.5% of the total retail sales of consumer goods. Among the online retail sales of physical goods, food, clothing and consumer goods increased by 18.8%, 11.1% and 13.1% respectively.

It can be seen that for China, this year's consumption is very low. Except for the "high growth" caused by the base effect in the first three months, consumption in other periods has continued to decline, especially since entering the second half of the year. The consumption growth rate has stayed in the single digits. Since August, the growth rate has stayed below 5%. In particular, it is worth noting that the consumption growth rate in October and November this year has been lower than the consumption growth rate in the same period last year, during the time when the COVID-19 pandemic was still serious. Now that we have entered the winter season, with the continuous emergence of the COVID-19, the beginning of the spread of Omicron variant and the impact on international market demand, it is certain that this year's consumption will end in an unprecedented downturn, and it will continue until the first quarter or even the first half of 2022. It is worth noting that consumption supports half of China's economic growth, and therefore, a continued downturn in consumption will determine the underlying conditions of China's economic growth.

Figure 2: Year-on-year growth rate of total retail sales of consumer goods (%)

Source: National Bureau of Statistics website

In November, the added value of industries above scale increased by 3.8% year-on-year, up 11.1% over the same period in 2019, and an average increase of 5.4% in the two years. From a month-on-month perspective, the added value of industries above scale increased by 0.37% in November over the previous month. From January to November, the added value of industries above scale increased by 10.1% year-on-year, and the two-year average increase was 6.1%. It should be noted that the industrial production sector has recovered better in the post-pandemic China and it is driven by both domestic and foreign markets. The growth rate of industrial added value slowed significantly in the second half of this year, which was only half that of the same period last year, indicating that it is the sector in China's economy that has rebounded the strongest after the pandemic, though its sustained growth vitality has been rapidly decreasing.

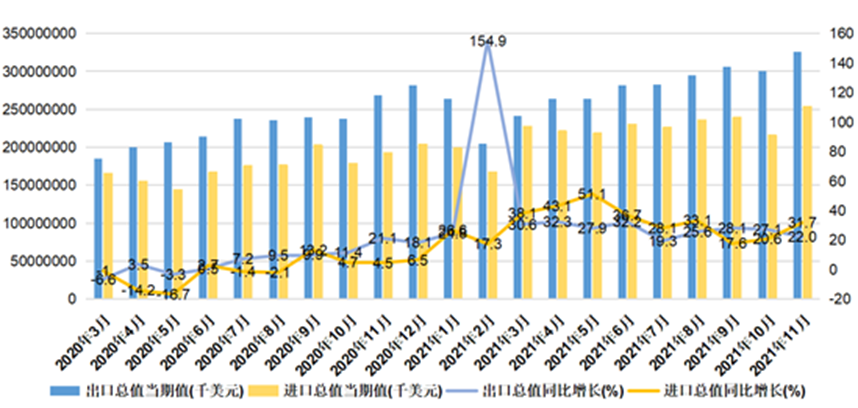

The import and export sector is the most dynamic part of China's economy this year, and has maintained a double-digit year-on-year growth so far this year. If calculated in the U.S. dollar, China's imports and exports have increased by 26.1% year-on-year in November this year. Among them, exports increased by 22% year-on-year and imports has seen the rise by 31.7% year-on-year. In the first 11 months of this year, the total value of China's imports and exports was USD 55.47 trillion, an increase of 31.3% year-on-year. The trade surplus was USD 5581.71 billion, an increase of 29.8% year-on-year. The rapid growth of export has not only boosted the overall economy, but also supported the renminbi to maintain a strong exchange rate against the U.S dollar, and effectively supported the stability of China's foreign exchange reserves. However, one should be aware that the high growth of China's export is related to the global production capacity internationally that has been affected by the pandemic, which can be regarded as a kind of "dividend". The sustainability of this "dividend" in 2022 will depend on the world's recovery from the pandemic.

Figure 3: China's monthly import and export scale and year-on-year growth rate

Data source: General Administration of Customs of China

In fact, this year's Central Economic Work Conference has made a clear judgment and objective statement on the downward pressure on China's economy, that is, the judgment of "threefold pressure of demand contraction, supply shocks, and weakening expectations". The current situation in China is related to the background of the complex and severe international situation, the spread of COVID-19 globally, the poor circulation of the industrial chain and supply chain, the rise in commodity prices, and the prominent domestic phased structural problems, and the emergence of new downward pressures on the economy.

National Bureau of Statistics spokesman Fu Linghui frankly admitted the impact of "threefold pressure". In terms of demand, the year-on-year growth rate of total retail sales of consumer goods has fallen from double-digit growth at the beginning of the year to single digits, and the two-year average growth rate has also fallen from 6.3% in March to 1.5% in August, which is still at a low level. The year-on-year investment growth rate has also fallen from double-digit growth at the beginning of the year to single-digit growth, and the two-year average growth rate has fallen as a whole, indicating that demand is shrinking. On the supply side, international commodity prices are rising, some domestic energy and metal supplies are tight, and the shortage of cores in some industries such as automobiles, has a significant impact, and the ex-factory price increases of industrial producers have continued to expand. The Producer Price Index (PPI) rose from 0.3% in January to 13.5% in October and remained at a high level in November. In terms of expectations, the manufacturing PMI has fallen continuously since April, and fell into a contraction range in September and October. Among them, the small business manufacturing PMI has been in a contraction range for seven consecutive months. The business activity index of the service industry as a whole also showed a downward trend. Among them, the business activity index of accommodation, catering and other industries all fell back to the contraction range.

According to the economic data of the past 11 months, the downward pressure on China's economy is increasing and uncertainty is growing, therefore achieving stable growth is not only the focus of the country this year, but also the top priority of next year. This is the realistic background of the Central Economic Work Conference's proposal to "take the lead in stability and make steady progress" under the "threefold pressure.

Final analysis conclusion:

The November economic data further revealed the pressure facing China's economy. The "pressure pattern" determined in 2021 will essentially continue into 2022 and exert pressure on China's economy next year. After the base effect caused by the COVID-19 pandemic disappears, the challenge of steady growth and risk resistance in the first half of 2022 will be particularly daunting for the country.