In the current geopolitical environment, climate change is a rare issue that has the potential to promote global cooperation, and China is a special and influential presence in this issue.

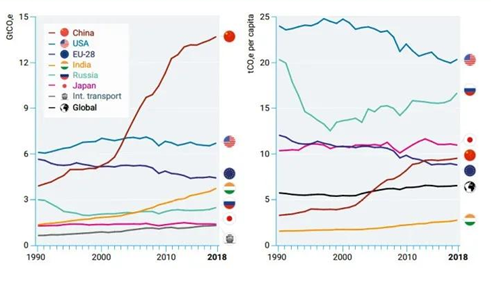

China is the world's largest emitter of greenhouse gases. Global greenhouse gas emissions reached 52 gigatons of CO₂ equivalent in 2019, an increase of 11.4% over the past decade, according to research by Rhodium Group, a New York-based advisory firm. For the first time, China's emissions exceeded 14 gigatons of CO₂ equivalent, or 27% of the global total. The United States was the second-largest emitter, accounting for 11%; India was third with 6.6%. China's "dual carbon" target (i.e., to peak carbon dioxide emissions by 2030 and achieve carbon neutrality by 2060) proposed in September 2020 has received many positive responses from the international community. After all, the fact that the largest carbon emitter has joined the global effort to reduce emissions and made clear commitments is an important step forward in the global effort to reduce emissions.

To curb climate change, an economically sustainable approach and mechanism will be indispensable, and the establishment of a carbon sink market is an important part of that. From the perspective of environmental economics, the negative externalities generated by greenhouse gas emissions need to be "internalized" by economic methods, so that free carbon emissions can be turned into paid activities, so as to curb carbon emissions. The carbon sink market and trading are one such mechanism. The so-called carbon sink refers to the process, activity, and mechanism for removing or reducing carbon dioxide from the air. What is traded in the carbon sink market is the commoditized carbon dioxide emission rights. Just as price is important to the market, the carbon sink price is a critical indicator in the carbon trading market. Generally speaking, carbon sink price can be considered as the price of carbon dioxide emission right in carbon trading.

The current global price of carbon sinks is highly volatile, ranging from the lowest of USD 1/ton of CO₂ equivalent to the highest of USD 120/ton of CO₂ equivalent as of 2020, but nearly half of the carbon emissions covered by carbon pricing mechanisms are priced at less than USD 10 per ton, with less than 5% of those carbon prices at levels consistent with the goal of the Paris Agreement. The Stern/Stiglitz High-Level Commission on Carbon Prices sees the price of carbon sinks in line with the Paris Agreement's temperature goal at USD 40 - USD 80/ton in 2020 and USD 50 - USD 100/ton in 2030. On this basis, sink prices are estimated to rise by 25% over the next decade. The latest European carbon sink price is EUR 50/ton, equivalent to RMB 388.88/ton, while the carbon price in Shanghai is only RMB 41/ton, and the price in Fujian is only RMB 15/ton. Therefore, it is believed that China's carbon sink price will have a lot of room to rise.

Since last year, there has been a surge of interest in climate change in China. With the proposal of "dual carbon" target, carbon trading, carbon emission reduction, and carbon reduction technology have become hot issues in policy and the market. Venture capital or equity capital, which used to be keen on the Internet industry, are now turning to carbon trading and green finance. At the recently concluded G20 Rome Summit, President Xi Jinping, on behalf of China, said that China will introduce plans and support measures to peak carbon emissions in key sectors and industries in succession, and put in place a "1+N" policy system to peak carbon emissions and achieve carbon neutrality. China will continue to transform and upgrade the energy and industrial structure, promote the research and development and application of green and low-carbon technologies, and support local governments, industries, and enterprises where conditions permit to take the lead in reaching the carbon peak. Some state-owned enterprises have vowed to reach the carbon peak ahead of schedule. The State Power Investment Corporation, for example, previously announced its goal of peaking carbon emissions in China by 2023. Some local governments also said they would strive to reach their carbon peak targets ahead of schedule.

With the national target of "dual carbon", the domestic market has become much more enthusiastic about carbon trading. Banks are thinking of promoting green finance to catch up with new policies; carbon emission reduction and new energy have become hot issues in the stock market. As well as thinking about the pressures of carbon reduction, entrepreneurs are also thinking about how to exploit the opportunities presented by "dual carbon" target. These issues are also reflected in the market's expectations of higher carbon sink prices.

However, the reality may not be so rosy. Researchers at ANBOUND believe that global cooperation on climate change is not always without hiccups, as the global carbon sink market is not built and does not operate as smoothly as expected. In view of China's carbon sink market, Chan Kung, founder of ANBOUND, even judged that in a complicated situation, one scenario cannot be ruled out, that the country's carbon sink price may plummet.

The first reason is that China's proposed carbon-reduction target may not satisfy industrial countries. China recently announced the Action Plan for Carbon Dioxide Peaking Before 2030, which sets out the following targets: "By 2025, the share of non-fossil energy consumption should reach 20%, energy consumption per unit of GDP should be reduced by 13.5% compared with 2020, and carbon dioxide emission per unit of GDP should be reduced by 18% compared with 2020... By 2030, the share of non-fossil energy consumption should reach around 25%, and carbon dioxide emissions per unit of GDP should drop by more than 65% compared with 2005". From China's point of view, great efforts have been made to come up with such a target, which shows China's good faith. However, from the perspective of developed countries, such targets are not significant compared with peak carbon countries, and peak carbon countries may not be satisfied with it. This disagreement could lead to greater climate pressure from developed countries on China, enough to create huge disruption for the Chinese economy.

The second reason is that the conflict between Western countries and China over climate change is likely to deepen. Historically, global warming is not only a common crisis facing the world, but also an issue concerning the right to development of both developed and developing countries. There are great differences in the time when countries in the world reach the carbon peak. There are 19 countries in the world that have reached the carbon peak before 1990, and their total emissions account for 21% of global emissions. Before 2000, 33 countries reached a carbon peak (including the countries that reached a carbon peak before 1990); a total of 49 countries peaked before 2010, accounting for 36% of global emissions. China aims to peak its carbon emissions by 2030, about 20 to 40 years later than these countries. China has a population of more than 1.4 billion and is still in the process of development. It is an extremely difficult task for China to reach its carbon peak within the next nine years. Judging from the current situation, western countries are unilaterally demanding China to pay a heavy price for climate change without providing corresponding economic and geopolitical compensation, regardless of the fact that "China is an important partner in the field of climate change mitigation". In an environment of geopolitical "hostility", Western countries could also blame China for global inflationary pressures if its low-carbon policies affect supply chains.

Total CO₂ emissions by major carbon emitters (left) and per capita emissions (right)

Source: Rhodium Group

Final analysis conclusion:

As things stand, China's Action Plan for Carbon Dioxide Peaking Before 2030 is a preconditioned action plan that depends on geopolitical and diplomatic progress in various aspects. While countries around the world are promoting cross-border carbon pricing, the global deep divisions in the field of climate change, the conflicting interests of developed and developing countries on climate change issues, and the increased penetration and influence of geopolitical factors on climate change issues are enough to cause a plunge in the seemingly optimistic carbon sink prices in the Chinese market.