In the post-pandemic period, China's economy has shown strong resilience and made a strong recovery from last year, bringing optimistic prospects for economic growth this year. However, from the current changes both in China and other countries, the overall macro economy will face a more complex situation in the second half of the year. Under such circumstances, the pressure and challenges of financial risk prevention will be more important in the second half of the year. For enterprises and government departments, they should avoid blind optimism and adjust their strategies and development layout.

As for the overall economic trend, researchers from ANBOUND have pointed out that after the recovery of the Chinese economy, the country faces structural problems such as limited household consumption, sluggish growth of manufacturing investment, employment pressure, while the momentum of economic growth is getting sluggish. This means that the trend ahead will be more challenging once the economy has recovered effectively from the pandemic. As for the situation in the second half of the year, policy officials from the People's Bank of China (PBoC) and the National Development and Reform Commission (NDRC) have repeatedly said that China's economic growth this year will be high at the beginning of the year, while it will be lower afterwards. In the case of a moderate rise in inflation and the "normalization" of monetary policy, China's financial market will face a buoyant trend for a period of time. For the macro economy under high leverage, the second half of the year there will be the challenge on rising financing costs. Maintaining the stability of financial markets and preventing the emergence of systemic risks will be the main tasks in the second half of the year.

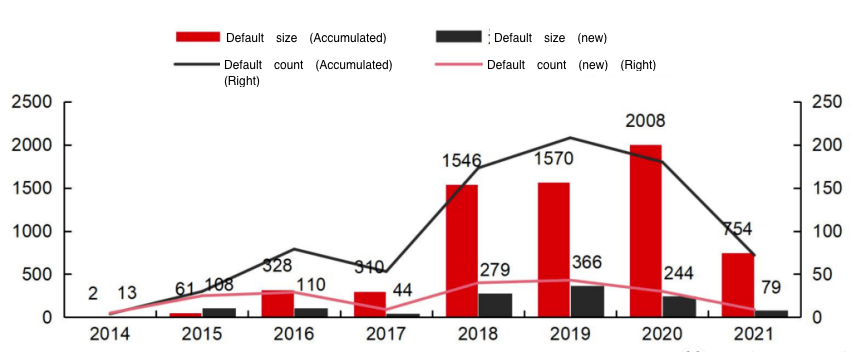

Figure: Scale and number of domestic credit bond defaults

Note: Data for 2021 are as of April 30, 2021

Sources: Wind, CITIC Securities.

In terms of the bond market, the credit default situation this year is still severe. According to research by CITIC Securities, as of April 30, the amount of defaulted credit bonds in 2021 totaled RMB 75.4 billion, and the number of cumulative defaults was 72. New first-time defaulters involved a default size ofRMB7.9 billion, and the number of defaults was 9. As of April 30, 2021, cumulative defaults were more than a third of last year's total, and first-time defaults were nearly a third of last year's total. In particular, the default risk of local state-owned enterprises (SOEs) is still accumulating after the default of Yongmei Group at the end of 2020. According to the statistics of CITIC Securities, as of April 30, 2021, among the enterprises that had defaulted for the first time, the number of private enterprises defaulted was 2, while the number of local SOEs defaulted was 5, involving a default size of RMB 5.2 billion, accounting for 66.15% of all defaulted bonds in 2021. The default risk of local SOEs increased significantly and became the focus of attention in 2021. It is worth noting that not only private enterprises are involved in bond defaults, there are also SOEs, local urban investment enterprises, and listed companies, which means that the risk is being transmitted along the credit financing chain, reflecting the continuous accumulation of credit risks.

As for shadow banking, which is more reflective of the real economy, non-standard defaults have also been on the rise this year. Data from Essence Securities showed that a total of 319 non-standard products defaulted from January to May 2021, with a monthly average of 63.8, higher than that in 2020 (59.7) and lower than that in 2019 (83.2). In terms of product types, the defaulted non-standard products in 2021 are mainly trust plans and private equity funds. Among them, there are 25 defaulted non-standard products with implicit government credit, accounting for 10.3% of all defaulted non-standard products, down 1.8 percentage points compared with 2020. Default urban investment is mainly distributed in Guizhou, Yunnan, Henan, Inner Mongolia, and Tianjin. From 2019 to 2021, the non-standard defaults of SOEs accounted for 21.2%, 21.0%, and 24.1% respectively, showing an upward trend. Non-standard defaults in the real estate industry rose significantly. In 2021, there were 33 non-standard defaults in the real estate industry, accounting for 15.6%, an increase of 7.6 percentage points compared with 2020.

In terms of the banking sector, the overall situation has improved in the short term, driven by loose liquidity and stimulus policies last year. The non-performing loan ratio has decreased in the first quarter of this year, but this was the result of policies that strengthened the disposal of non-performing assets last year and the extension of credit to small and medium-sized enterprises. The impact of the pandemic, in fact, has a greater impact on small and medium-sized banks, and the pressure on them will be even greater in the future.

Overall, the continuous accumulation of domestic credit risks indicates that the financial risk prevention in the second half of the year will be more challenging, which involves not only the risks of small and medium-sized enterprises and private enterprises, but also the risks of SOEs and local governments. The accumulation of credit risk is no longer a cyclical problem or a liquidity problem, but more of a deeper structural problem such as economic structure, industrial structure, and financing structure. In terms of long-term structural problems, Gao Shanwen of Essence Securities believes that in recent years, the decline in domestic investment returns and the rise in interest rates are the main factors that constitute the rising credit risk. He stressed that the most important impact is that the government has treated the economic decline as a cyclical phenomenon over the past decade and thus believed that the market needed a lot of fiscal support, leading to massive public sector financing in the market. However, the aggregate demand for public sector financing expansion is subject to weak interest rate constraints, which pushes up interest rates and crowd out private investment.This leads to the paradox of economic decline and rising interest rates. The more severe the private sector crowding out, the stronger the public sector economic expansion, which in turn forming a vicious circle.

In this regard, in the second half of the year, as the financial risk prevention pressure intensifies, there is still a need to pay more attention to structural reforms from a policy perspective, focusing on the balance between adjustment and expansion. In terms of fiscal policy, with the scale of fiscal spending decreasing in the first half of the year, there is a need to focus on fiscal sustainability in the second half of the year, especially the sustainability of local debt. In terms of monetary policy, we believe that monetary policy can be moderately loosened to maintain the stability of the financial system as the Fed begins to tighten U.S.' monetary policy. As for the local governments, the model of economic development needs to be adjusted to avoid expansion in conventional areas, as well as focusing on the cultivation of market players. For enterprises, the way to rely on scale expansion will be increasingly limited in the future, and it is necessary to pay attention to the investment in scientific research and the integrity of industrial chain support. All in all, the focus in the second half of the year is still on stabilizing leverage and avoiding financial risks from getting out of control.

Final analysis conclusion:

China's economy, which recovered relatively quickly in the post-pandemic period, faces a more complex internal and external situation in the second half of the year, and needs to face the accumulation and increase of anti-risk pressure. Stabilizing leverage and adjusting structure will be the theme of policy adjustment and business development for China in the second half of the year.