As commodity prices continue to rise in the post-pandemic economic recovery, the issue of inflation has become a focus of debate and concern in both the market and academia. On the one hand, from a global perspective, the global economic recovery has brought about rising energy and raw material prices, which has strengthened global inflation expectations. On the other hand, rising domestic raw material prices in China have pushed production prices to record highs, which could feed through to the consumer market and raise fears of "stagflation" in the face of slowing economic growth. Inflation has become the biggest concern for China's economic recovery and growth in the second half of the year.

Source: Qidian Caijing.

Economic data for April showed a slowdown in industrial production, consumption, and investment growths, while the production side, including imports and exports, is still growing much faster than the consumption side. According to the National Bureau of Statistics, the value added of industries above designated size grew by 9.8% year-on-year in April, down 4.3 percentage points from March; the two-year compound average growth rate was 6.8%, unchanged from the first quarter. The total retail sales of consumer goods in April increased by 17.7% year-on-year, down 16.5 percentage points compared with March; the two-year average growth was 4.3%. Fixed asset investment in April grew 9.9% year-on-year, down 8.4 percentage points from March. In the January-April period, fixed asset investment grew 19.9% year-on-year, with a two-year compound average growth rate of 3.9%. Therefore, although China's economy posted a rare surge in growth in the first quarter, it is more or less due to last year's low base effect, and there are concerns about its sustainability.

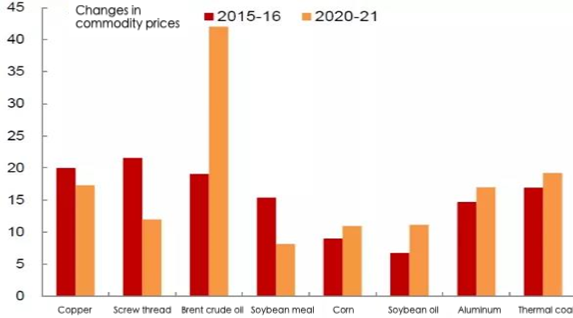

Some scholars and research institutions tend to believe that the CPI slump in the face of higher PPI reflects a widening gap between the two price indexes. The PPI rose to 6.8% year-on-year in April, the highest since October 2017, while the CPI rose 0.9%, less than expected. As a result, many are worried that the current recovery in demand will be insufficient. The production side has seen increase, while the demand side is still stagnant. Under such circumstances, many people are concerned that the high PPI will be transmitted to the consumer market over time, bringing a rapid rise in CPI and forming a "stagflation" dilemma.

In the view of ANBOUND's researchers, this concern stems from the logic of inflation in conventional economic theory. However, the evolution of the global economy, including China's, has changed so much since the 2008 financial crisis that a new perspective is needed to understand the evolution of inflation. In the economic cycle since 2008, on the one hand, the new technology has brought about the improvement of production efficiency and the prosperity of the new economy, forming new "artificial" demand. On the other hand, the expansion of the financial system under monetary easing has pushed up asset prices, making the transmission chain of inflation from money supply to the real economy longer. These two factors have led to a change in the conventional pattern of inflation transmission.

Although the current PPI is at a historical high level, it is difficult for CPI to grow too fast when the overall consumer demand has not recovered strongly, and most of the inflationary pressures will still be absorbed during the process of asset trading and the production process. Therefore, inflationary pressures will have limited negative effects on the economy when the overall monetary policy returns to a neutral stance and the liquidity margin shrinks. From a micro perspective, this situation brings a lot of pressure to businesses. Higher prices of raw materials raise business cost, while the weak consumption makes it difficult for businesses to raise prices, which means that businesses will have to absorb the cost pressure. This leads to intensified competition, pushes for industrial restructuring and market-oriented "overcapacity reduction". Such situation also has an impact on imports and exports, and some central bankers even hope that exchange rate appreciation will help companies offset the pressure of rising imported commodity prices. This situation is a long-term consequence of overcapacity. As a result, it is expected that corporate debt will continue to rise, non-performing assets of financial institutions will increase, and market divergence and the "asset shortage" in the capital markets will intensify. This change indicates that the "rise" of the financial market and the "stagnation" of the real economy exist simultaneously.

ANBOUND has previously mentioned that the space and effect of macro policy adjustment in the future will become very limited with the aggravation of structural contradictions. Neither monetary policy should be eased to bring inflation, nor tightened to burst asset bubbles. It should be noted that the post-pandemic economic environment is different from that in the post-financial crisis era in 2008. As noted by Morgan Stanley researchers, the global economy is in a critical period and it is facing a very different risk situation. Over the past decade, the risks to the economy tended to be to the downside, with the suspense over what new forms of easing central banks would come up with to counter the slowdown, while the new challenge is to maintain room for growth amid economic recovery and adjustment of the global industrial chain. Despite the uneven recovery of the global economy in the post-pandemic period, China's overall economic situation remains highly resilient. As a result, China's economy still has the potential to grow amidst the "stagflation".

Under the new circumstances, China needs to focus more on structural reforms and layouts in its policies, including encouraging technological innovation and optimizing capital market reforms to expand new market spaces in new strategic areas such as the digital economy and green economy. At the same time, the capital market should be optimized and improved to play its role as an investment pool, and the inflationary pressure should be alleviated by improving the efficiency of investment and production.

Final analysis conclusion:

After a rapid recovery from the COVID-19 pandemic, China's economy is facing a new situation of "stagflation". This situation not only poses new challenges to the country's future development, but also differs from the conventional economic pattern. Therefore, China needs to be fully aware of this situation when formulating macro and micro policies and seek to create new development pattern through promoting structural reforms.