In the post-pandemic period, the global economy has shown a diverging trend of "K-shaped" recovery. On the one hand, China and the U.S., through different means of prevention and control of the pandemic, are effectively controlling the pandemic and promoting a rapid recovery of economic activities. Europe, Japan, and most emerging markets are still hampered by the pandemic and are recovering slowly. A recent article in The Economist noted the new geopolitical shift in global business, suggesting that China and the U.S. have reached an "unprecedented" level of dominance. Despite the article's concerns, the way it looks at the evolution of global business and enterprise is noteworthy.

The article pointed out that one way of capturing the dominance of the U.S. and China is to compare their share of world output with their share of business activity (defined as the average of their share of global stock market capitalization, public-offering proceeds, venture-capital funding, "unicorns" or larger private startups, and the world's biggest 100 enterprises). By this yardstick, the U.S. accounts for 24% of global GDP, and 48% of business activity; China accounts for 18% of GDP, and 20% of business activity. Other countries, with 77% of the world's population, account for a much smaller share of global GDP and business activity than the U.S. and China.

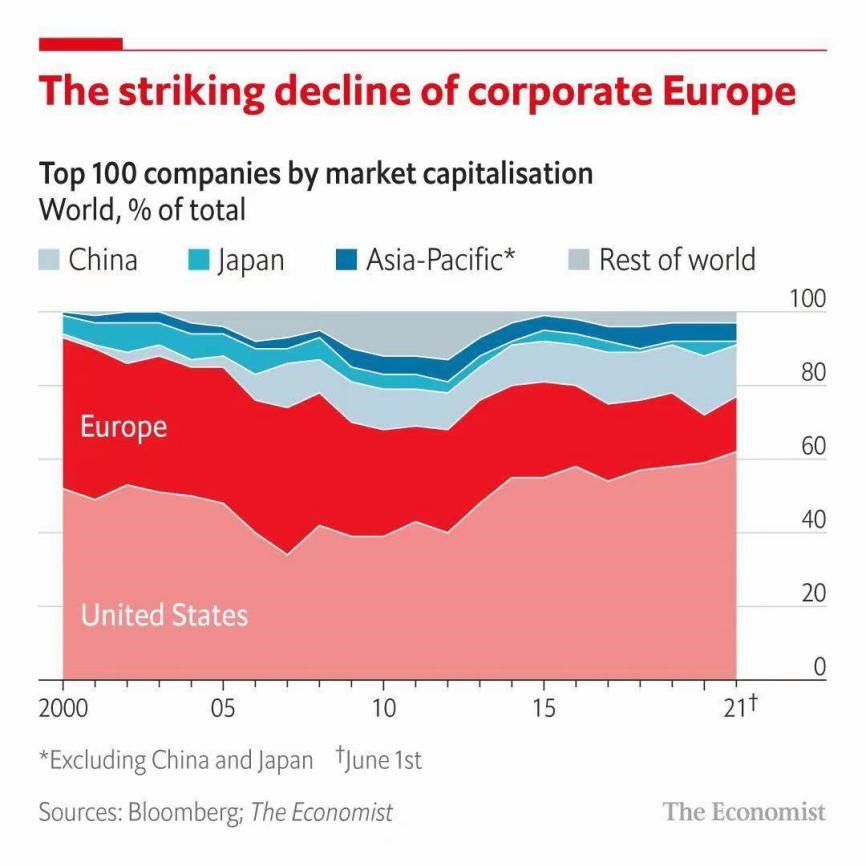

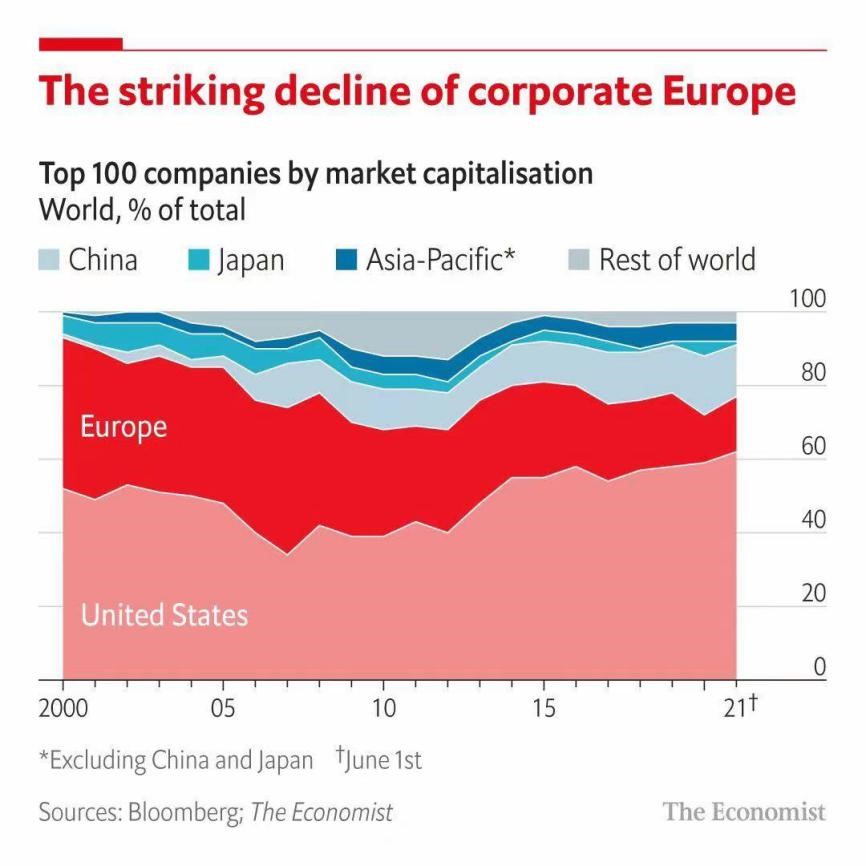

Figure: Top 100 companies by market capitalization in major economies

Sources: Bloomberg; The Economist

The changing landscape of large global corporations actually reflects the rise and fall of economic activity in each country. In the view of researchers at ANBOUND, it is the technology and the tendency to "capitalize" the economy amid monetary easing around the world that have brought about this change. The Economist calls this shift in technology and business models "creative destruction". In fact, since the 2008 financial crisis, the global economy, driven by high-tech innovation, has become increasingly virtualized. At the same time, the evolution of the ability to capitalize currency in the context of widespread overissuance of money is leading to changes in the global economic pattern.

Based on these changes, The Economist pointed out that it is this pattern of "creative destruction" that has led to a highly uneven regional integration. The U.S. and, increasingly, China are ascendant, with both countries owning 76 of the world's 100 most valuable companies. Europe's tally has fallen from 41 in 2000 to 15 today. The article also pointed out that European companies generally failed to anticipate the change toward the intangible financial system. Europe has no startups that can rival Amazon or Google. Other countries are also struggling. A decade ago, Brazil, Mexico, and India were all expected to create a massive cohort of multinational companies, but few were successful. This "creative destruction" model succeeds in two ways. The first is that a large domestic market helps companies achieve economies of scale quickly. Second, capital markets, networks of venture capitalists, and top-tier universities provide a steady stream of money, talent, and technology for start-ups.

While this view does have some merit from a corporate perspective, it ignores the impact of the trend of "capitalization of currency". The report on Global Industrial Chain Restructure and China's Choices by China Finance 40 Forum also believes that with the change of global factor endowment pattern, the global industrial chain will show the trend of knowledge-based, digitalized, and capitalized in the medium and long term.

In terms of the capitalization degree of companies in major countries and regions in the world, the U.S. is still in dominant position, and its influence is still increasing with its QE policy; China also contributed to the increase in capitalization after 2008 by issuing large amounts of currency. The continuous development of the stock markets in the two countries has brought about momentum to currency capitalization, as well as the rapid expansion of enterprises and the improvement of economic power. Europe, Japan, and other economies are gradually "falling behind" in this process. The main reason is that their conventional indirect financial system, which is dominated by the banking industry, causing businesses not turning money into capital, but continuously increasing corporate debt in the process of economic financialization. This in turn drags down the potential of economic growth. The U.S., through its well-developed stock market, has been able to finance a large amount of capital for enterprises and convert sovereign debt well into corporate capital, thus taking the lead in global competition. In China, while the conventional financial model still accounts for a large amount of financial resources, some emerging technology enterprises also raise a large amount of capital in the United States or Hong Kong, realize the process of capitalization, and become internationally competitive enterprises. Chinese financial officials have also repeatedly talked about "replacing the indirect financing model with the direct financing model", promoted the opening of the Science and Technology Innovation Board, the reform of the A-share market, and also promoted currency capitalization with the expansion of the capital market.

The past development trajectory not only represents a trend, but also indicates a direction for the future, which is of particular significance for China's future development. ANBOUND believes that in the era of credit expansion and excess capital, the ability of enterprise capitalization is actually the ability to obtain various resources. It's a new kind of competition. The scale of China's current M2 money supply is already twice that of the United States, while the driving GDP level is only 60% of that of the United States. This means that China still needs to promote the capitalization of currency to realize the effective allocation of financial resources and reduce the level of corporate leverage. This could represent a new shift in the model of economic development.

Final analysis conclusion:

In the process of global monetary easing and global industrial chain restructuring during the post-pandemic period, attention should be paid on the trend of digitalization and capitalization of economic development. This could represent a shift to a new model of economic development and a new approach to monetary and fiscal policy.