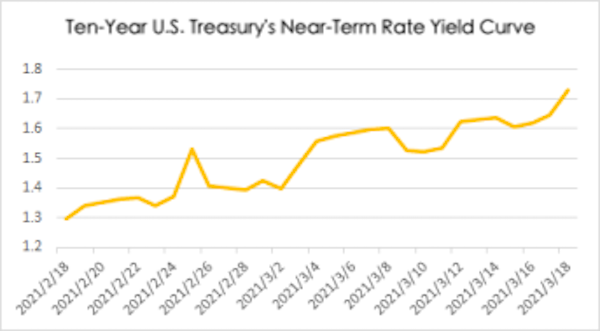

Due to rising inflation expectations, the Federal Reserve's monetary policy meeting has attracted attention from global capital markets. Although the Federal Reserve's latest policy resolution clearly stated that the current easing policy will continue, and that it will not initiate interest rate hikes before 2023. Yet, the Fed is still unable to win the trust of the capital market as "inflation trading" continues in the capital market. On the 18th of March, the yield on the 10-year U.S. Treasury bond rose above 1.7%, and the U.S. dollar continued to strengthen. At the same time, U.S. stock futures continued to fall. These results indicate that the U.S. central bank and market investors are still gambling with each other, and the Fed's determination in easing the policy has not won the trust of the market. The challenge for the Fed's future policy lies not only in its ability to achieve its policy goals, but also in its ability to win the trust of the capital market.

After the Fed's monetary policy meeting, Fed's chair Jerome Powell made it clear that he would stick to a loose monetary policy for a period of time but predicted that the economy will see a strong recovery and inflation will rise above the target level. The Fed also predicts that the U.S. economy will grow by 6.5% in 2021, the largest annual GDP growth since 1984, a sharp increase from the 4.2% forecast that was made just three months ago. It expects the unemployment rate in the United States to fall from the current 6.2% to 4.5% this year, exceeding the 5% forecast in December last year. Concerning the level of inflation which has attracted the most attention from the market, the Fed expects that the U.S. core inflation will rise. The PCE inflation expectations in 2021, 2022, and 2023 are 2.4%, 2.0%, and 2.1% while the personal consumption expenditures (PCE) price index expectations for those years are 2.2% and 2.0%, and 2.1% respectively, both higher than last year's expectations. This shows that the expectations of rising inflation in the United States have become the consensus of policy departments and market institutions. The only difference is that the Federal Reserve believes the inflation to be moderate and within policy tolerance, while the market is worried that the inflation would lose control and cause monetary policy to change its direction.

The market's worries and disagreements are actually caused by a lack of confidence in the Federal Reserve's future policies. The Fed's new policy framework for adopting average inflation expectations in particular has not been tested in practice, hence policy confidence has not yet been established. Many economists worry about the fact that Powell has repeatedly emphasized that the Fed will not raise interest rates until the U.S. economy sees a full recovery from the COVID-19 pandemic, showing that the policy tone is actually different from the conventional basic principle of monetary policies which is taking preemptive measures against inflation. By increasing yields in recent weeks, the market is actually testing the new monetary policy framework implemented by the Fed. Whether the Fed is willing to increase the purchase limit of treasury bonds and conduct yield curve control operations will be a reference for the market to observe the direction of the Fed's policy.

In addition, the market is very concerned about the changes in the dot plot without getting an effective explanation from Powell. Powell does not seem to care much about the Fed's interest rate outlook. Instead, he emphasized that most policy members insist on the view of zero interest rates. However, the dot plot shows that among the 18 Fed officials, 7 expect interest rates to rise by the end of 2023. Comparatively, only 5 of them held this view at the end of the last meeting. In addition, an analyst at Nordea stated in a research report that 4 of the 18 Federal Open Market Committee (FOMC) members believe that interest rates will be raised in 2022, compared to only 1 in December last year. In fact, the changes in interest rate level expectations are slowly accumulating, making the market worry that this "quantitative change" trend will bring "qualitative changes". The market is even more worried that the rapid rise in inflation may force the Fed to raise interest rates.

Of course, various institutions now have increasingly differing opinions on the future of inflation and the direction of the capital market. The increase in these differences means that the capital market's expectations for the future as well as the degree of trust in the Federal Reserve's monetary policies are changing. It also means that the future capital market will experience greater fluctuations as the U.S. economy improves. This is the inevitable consequence of the flood of liquidity under the Fed's super-loose policy. At the same time, European Central Bank President Christine Lagarde also said that short-term inflation can be tolerated in order to stabilize economic recovery. This shows that the world's major central banks still hope to achieve economic and employment goals before high inflation occurs. Yet from another perspective, this also means that the rise in global inflation will be a major trend in the future which is not necessarily a good thing for the capital market.

Judging from the recent changes in the capital market, on the one hand, the increase in inflation expectations has led to the sell-off of long-term bonds; on the other hand, the tech stocks that grew faster last year are in the callback, while prices of cyclical financial stocks and consumer stocks that are expected to be benefited from the economic recovery are rising. These structural changes in the capital market are actually the self-adjustment of the capital market in the context of increased policy uncertainty in the future.

Therefore, although the Fed has repeatedly insisted that its loose policy will remain unchanged with the hopes that such statements would calm the market, the implementation of the new round of stimulus policies in the United States as well as the increase in dollar liquidity is causing concerns regarding inflation and changes in the Fed's policy. Such concerns too, are exceeding the optimistic expectations for economic recovery. From this point of view, whether it can win the confidence of the market and maintain a balance between economic growth and inflation is the biggest challenge for the Fed's future monetary policy.

Final analysis conclusion:

Although the Federal Reserve has insisted that it will keep monetary policy loose, this has failed to completely dispel the fear in the capital market. The market's confidence in the Fed is still fragile and sensitive, therefore future fluctuations in the capital market can be expected to be volatile.