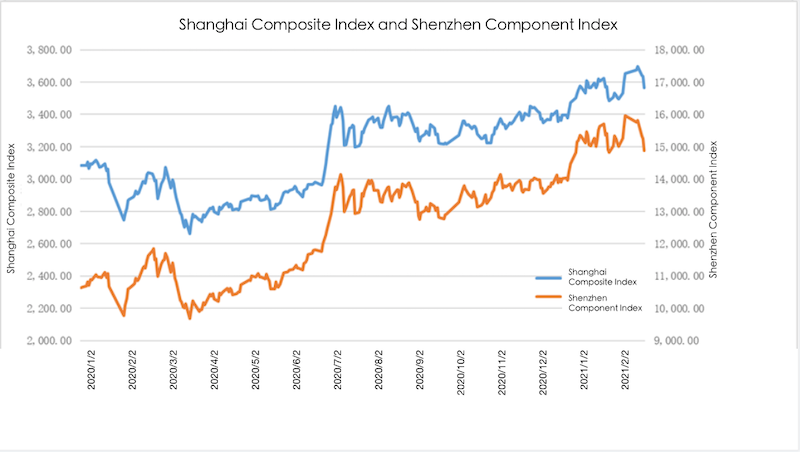

Under the influence of variegated factors both domestically and internationally, the three major A-share Indexes in China fell sharply on February 24, among which the Shanghai Composite Index fell 1.99%; the Shenzhen Component Index fell 2.44%; ChiNext dropped 3.37%. The Shanghai and Shenzhen bourses traded a total of RMB1.06 trillion. The stocks under institutional investors' concentrating investment, led by the brewing sector, fell heavily. After the Spring Festival (i.e., Chinese New Year), the Shanghai Composite Index reached a high of 3731 on February 18, and after significant fluctuations, it began to fall significantly. In particular, public offering funds and other institutions have seen a decline. These sharp fluctuations reflect the fragility of the capital market and investors' apprehension.

It should be noted that since last year, one of the main factors for the rise of foreign capital markets in China is the result of U.S. monetary stimulus. With the real economy being hit by the COVID-19 pandemic, a large amount of fund unleashed by monetary policy is seeking policy benefits in the capital market. Despite the apparent enthusiasm of investors and the fact that stock indexes around the world are hitting record highs, this phenomenon has left global capital markets extremely vulnerable. The debates over inflation expectations and changes in the price of Bitcoin show that investors were merely seeking for some certainty to keep the market buoyant.

In the case of the U.S. stock market, the concern is now rising amid a growing reflation trade, with tech stocks already in the midst of a pullback. As it stands, the market is particularly concerned about the U.S. government's stimulus policy and the Fed's monetary policy changes. Some statements from government officials and investment moguls could provoke strong market reactions. For example, Fed Chair Jerome Powell's comments on loose monetary policy have boosted market confidence and sent U.S. stocks higher. Powell and U.S. Treasury Secretary Janet Yellen have been emphasizing the accommodative stance in various ways to calm the markets, keep capital markets buoyant and provide an opportunity for the real economy to recover and grow.

The opposite was the case in Hong Kong. Shares in Hong Kong fell sharply on February 24 after the government announced unanticipated plans to increase the stamp duty on securities trading. This move has hit the Hong Kong stock market, which had a rare positive trend since last year. Hong Kong's Hang Seng index fell 2.99% to below the 30,000-point mark with a record daily turnover of HKD 353 billion. Such policy has brought a great shock to the market, and reflected the vulnerability of the Hong Kong stock market. While the return of Chinese companies once listed in the U.S. and the increase in southbound funds have brought about the prosperity of Hong Kong stocks, this kind of prosperity was not stable and sustainable. Under such circumstances, any policy moves would make the market "jittery". Therefore, any policy adjustment should to take this issue into account.

The same is true for the A-share market. At the beginning of this year, although the policy authorities have been emphasizing the prudent policy stance, the central bank's market operations in January have caused speculation, thus triggering significant volatility in the stock market. Recently, the Chinese stock market has also become increasingly vulnerable, as stock market indexes have risen and the phenomenon of institutional investors' "concentrating investment" has become increasingly serious. Despite the continuous strengthening of market regulation and the continuous improvement of the market environment, investors' expectations have not been strengthened along with the improvement of the economy. Instead, they have become more anxious and worried about the impact of policy changes. Since the beginning of this year, public offering fund's raising has continued the boom since last year. As of February 10, the scale of new funds established since 2021 has exceeded RMB 700 billion, and the fund issuance market is expected to continue this trend in March. These figures suggest that the market is not short of money, and that the stock market adjustment is a reflection of uncertainty brought about by policy factors and changes both within China and in other parts of the world.

In particular, Kweichow Moutai, a closely watched stock under institutional investors' concentrating investment, saw its price drop 5.11% on February 24, with RMB 517.553 billion of its market value wiped off in the five trading days after the Spring Festival. Although some institutions and funds have reduced their holdings of Kweichow Moutai, but in the case of "concentrating investment", Guizhou's state-owned assets are also deemed to be involved in the related operation. For two years in a row, the State-owned Assets Supervision and Administration Commission of Guizhou Province transferred the equity of Kweichow Moutai to the state-owned enterprises (SOEs) and "cashed out" the transferred equity by impairment. The revenue brought by equity transfer can make up the fiscal gap, so that the local government can obtain real income. However, from the perspective of the market, this kind of equity transfer will affect investors' expectations of the stock, which can set off a chain reaction. The continuous decline of Kweichow Moutai's stock price has even affected the performance of the funds and caused losses to the fund investors. As the mixed reform of SOEs is further promoted, this kind of equity transfer will certainly trigger market volatility and amplify the related negative impact.

The capital market will play an extremely important role in China's economic and social stability in the future. Researchers at ANBOUND pointed out that greater attention should be paid to the increasingly pivotal role of capital markets in China's economic development. As a matter of fact, there are two financial systems in China. SOEs, public finance, and local governments are deemed as the internal finance related to the system, while external finance refers to the foreign capital and capital market. As the regulator, the People's Bank of China (PBoC) is in a position that crosses the two sides. At present, public finance and local government finance are both in a very difficult situation, so the key to the improvement of economic structure, the development of science and innovation enterprises, and the mixed reform of SOEs still lie in the development of the capital market. At the same time, the increase of household wealth is also inseparable from the prosperity of the capital market.

This signifies that the development of the capital market is not only related to the financing of enterprises and government departments, but also indirectly affects consumption, investment, etc. Under such circumstances, whatever policies taken in the future must be conducive to the prosperity of the capital market. Otherwise, the collapse of the market will not only bring losses to investors, affect the stability of finance and enterprises, but also lead to financial and local government finance crises, causing the overall situation to be out of control.

Final analysis conclusion:

The recent Chinese and international capital markets have experienced volatility, while the Chinese A-share market has fallen sharply. This reflects the fragility of the booming capital markets. Under such circumstance, it is very important to maintain the prosperity of the market. This is also a factor that should be taken into account when promoting economic recovery and financial risk prevention.