Before the year 2015, proud of China's achievements, most Chinese including the elites did not believe that the crisis would happen, at least not that fast. Things have changed in the past two years, and many Chinese have started to rethink of the issues in front of them.

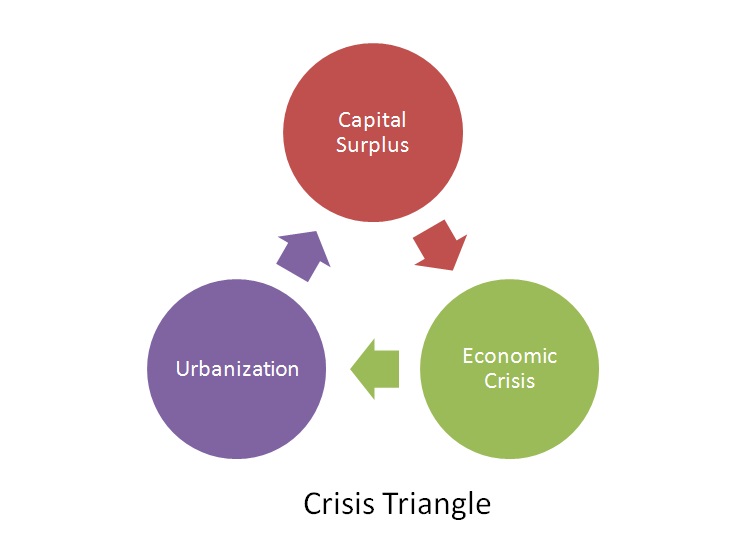

Taking the longue durée perspective, the book Urbanization: Cycle of the Crisis Triangle, written by ANBOUND chief researcher Chan Kung, observes the relationship between the world's urbanization wave, capital surplus, and financial crisis. The author put forward a model called "Crisis Triangle", based on the observations. With warnings on the dangers of global capital surplus, this book offers strategic analysis of the incoming crisis and questions the approaches taken by the governments worldwide in their promotion of urbanization, and even doubts on the goals of development economics.

This book covers development economics, economic history and urban studies from an inter-disciplinary perspective, with the target audience being scholars in these related fields.

Its Chinese version (ISBN 978-7-5086-5859-9) was published in 2016 by China CITIC Press in Beijing. The book is composed of 8 chapters, with the Chapter 8 of From Crisis Triangle to Utopia as below.

The capital bubble is an explanation of the current capital surplus under the economic framework. Such explanation has been in use from the time Paul Krugman began to touch this issue until now. The existing economics has consistently understated the root causes and mechanisms of the capital bubble, as if it is naturally formed and intensified by the people. Yet the real world is contrary with theories. The United States in 2008, China in 2015, and Europe now all have been in constant crisis. This is an organic, comprehensive worldwide crisis, a crisis of global capital surplus caused by urbanization. It first started with Europe because of "euronization", and the United States because of the new economy. Since then, it has expanded to the BRIC countries, then to the whole world.

How then, should the rebalancing of the global economy be achieved?

Excess capital is formed during the process of urbanization. The excess capital manifested by personal, group and government wealth, under the premise of free flow, has caused major fluctuations and shocks in the market, which would then trigger global crisis. Reducing and offsetting such excess capital is, for individuals, a loss of wealth, which of course is another issue, while for the world it is the response of the market order and the reappearance of real value. Reducing and writing off capital surplus, then is a challenge in the current global political and social environment, where the spirit of market liberalism is prevalent.

In his Capital in the Twenty-First Century, Thomas Piketty has put forward the concept of "capital tax", but he did not have much confidence, so he added a lot of "disclaimers". He first pointed out that this is a "useful utopia", and "[i]t is hard to imagine the nations of the world agreeing on any such thing anytime soon. To achieve this goal, they would have to establish a tax schedule applicable to all wealth around the world and then decide how to apportion the revenues[1] ." The fundamental purpose of the "global capital tax" proposed by Piketty is to break the dominance of financial capitalism, because his research focus is that capitalism is still creating an unfair economic environment. However, it is undeniable that despite the purposes are different Piketty's "global capital tax" is also helpful in reducing global capital surplus.

In order to achieve a rebalancing of the global economy, in addition to Piketty's suggestion, governments around the world are also making efforts, yet the results are often unexpected, such as wars and economic crises, inflation and deflation, as well as technological and financial innovations. To realize the global rebalancing that seems almost impossible is to achieve, it will inevitably involve the following three main approaches[2].

The first is the large-scale "discard and suspension" of tax debts and capital.

The method of taxation is like what Piketty and his fellow economists suggest; in addition to the "global capital tax", worldwide option can be considered in the issuance of global debt. The significance of global debt is to absorb excess world capital for international welfare, for the development of poor countries, and to reduce the possibility of war caused by poverty. There are indeed are some well-functioning financial institutions and organizations with worldwide and regional characteristics, such as the World Bank in today's world. If the political consensus can be reached, the possibility for the realization in the future is far greater than the "global capital tax".

The "large-scale discard and suspension" of capital means the halt of the enthusiasm of the world for development projects. This requires the global financial community to build a new perspective to look at currency finance development and face the tide of serious capital surplus caused by urbanization. Such thought does not have practical significance in many countries, but in some countries there are success stories. For example, in the 20th century China when Zhu Rongji assumed the premiership, administrative means were adopted to suspend the widespread "hot development zones" in China to stabilize the financial system. Although such a practice did cause some so-called "waste" of capital, in the long run it actually ensures the true value of the future market and laid the foundation for development. Therefore, the government experiment in China at the end of the 20th century can serve as a useful example for the world[3].

The second is the globalization of welfare.

According to the World Bank's World Development Indicators released on April 17, 2013, the average income of extremely poor people in developing countries began to rise continuously, steadily approaching the World Bank's daily poverty line of US$1.25. Between 1981 and 2010, although the population of developing countries had increased by 59%, the proportion of the poor living below the poverty line of US$1.25 a day dropped significantly from 50% to 21%. According to the report, the top three countries and regions that accounted for the world's extreme poor are sub-Saharan Africa, India and China. Among them, sub-Saharan Africa and India accounted for an increase in the proportion of the world's extreme poor in the past 30 years, while China's proportion dropped significantly from 43% in 1981 to 13%. World Bank stated that there are still 1.2 billion people in the world who are extreme poor. Despite the rapid decline in extreme poverty rates in many countries in recent years, the World Bank estimates that by 2015, there will still be 970 million people living on less than US$1.25 a day.

The success of globalization means there is the globalization of manufacturing and financial capital. Now the challenge for human society is that whether there will be the globalization of welfare, and if it could be distributed to every remote corner of the world. This is of course a difficult process, and it is extremely hard to achieve success in the face of conflicts between development levels and cultural environments. However, the globalization of welfare is of great significance, and it is not merely an act of financial distribution. Welfare globalization is not just an advocacy, but also a beneficial measure to improve the global capital environment. It can use the excess capital from production capacity to benefit the poverty-stricken corners of the world and put the natural resources that were originally exploited into better use. At the same time, it also reduces the danger of ethnic conflicts and even wars in the world.

The third is the worldwide currency reform.

Currency reforms usually include regional and local currency reforms. Effective regional currency can theoretically lead to a relatively consistent level of development, especially in avoiding excess capital caused by competitive monetary policy. Therefore, currency zone is an important currency reform direction in the future. Although the Eurozone is still struggling, it has the correct direction in its attempt. In particular, if the hidden dangers of the currency zone stimulating sudden increase in investment can be eliminated, even if it cannot solve the problem of eliminating capital surplus, such a currency reform will help to improve the problem.

A successful sample of currency reform can be found in Germany.

The post-Second World War Germany faced a large amount of capital surplus, manifested as inflation. In 1948, after the war the German economy fell into an extremely difficult situation. Due to the widespread destruction of the war, the manufacturing output was less than 60% in 1936, and the per capita actual consumption level was only about two-thirds of that in 1936; most of the daily necessities were seriously scarce. Moreover, war loan had made the Third Reich's public debt almost 400% of the 1939's GNP after the war, and led to a huge excess of liquidity. The Reichsmark (RM) lost its role as a means of exchange, and barter trade became a daily form of transactions, while black market trade gradually undermined prices, wage management, and commodity production-distribution systems. The mechanisms that could motivate people to work for money had vanished. Imported goods in the market would be sold out in split seconds, and foreign exchange earnings must be converted into the RM, which made exports unprofitable.

To solve this problem, American economists designed the famous Colme-Dodge-Goldsmith Plan for Germany. The genius designers of these financial policies noted that cash and demand deposits (M1) in the non-bank sector increased by nearly 500% between 1935 and 1945, while GNP fell by more than 40% during the same period. This sharp increase in the money supply was accompanied by the freezing of prices and wages and the implementation of the rationing system since 1939, with the result that a large excess of money had emerged. In order to return to the level of 1935, which was considered normal, M1 had to be decreased by 90%. Therefore, the designers of the financial reform proposed 1 German Mark to be exchanged for 10 Reichsmark[4], in order to change the price level at that time to a new, balanced one. The result of this monetary reform was unprecedentedly successful, and the German economy achieved an incredible renaissance and development after the war. In addition, the Bretton Woods Agreement was also part of the currency reform, and given the dangers of the real world, the future "new Bretton Woods Agreement" would also be an expected currency reform. Among them, like the original Bretton Woods Agreement, the governments of the world have much space to play their role.

The role of the government has long been questionable. In particular, believers in free competition, like those from the Austrian School regard the government as a beast while that the free market is omnipotent. Although things have always been two-sided, this provides people with a great space for interpretation. The same thing can always be explained from another logical point of view; however, it is the reality that the development of democracy in the world is unstoppable. In the predictable future, governments around the world will mutate into a social welfare organization. For a social development environment, especially the financial capital environment, such a large-scale social welfare organization is actually an indispensable backbone.

One needs to see the issue from a different perspective.

The role of the government in a society depends on paradigms and standards. In our world, there are indeed so-called "good" and "bad" governments. We can question the definition of "good" and "bad", but we cannot question the government as a public institution that is increasingly turning to social welfare organizations.

The key of the problem lies in the normative operation and various social standards; these are matters pertaining to political philosophy and they are decided by the stages of social development.

From the perspective of the Crisis Triangle, the government is the primary initiator; it is the originator of numerous capitals and investments, yet at the same time people had to pin their hopes on the government; this is because the mechanisms of free markets are sometimes unsuccessful. While the mainstream economics also recognizes market failures, they are mainly attributed to imperfect competition, external effects, insufficient information, transaction costs, and unreasonable conditional reasons, in addition to unfair income distribution and unbalanced economic fluctuations. The question is, can these conditions and factors be completely resolved by the free market? The answer to this question is clearly no, and hence this is where our expectations for the government as a "social welfare organization" [5]derived from.

In the real world, any businessperson would tell you that the bigger the better when it comes to chasing profits; the same goes for investment as well. This is the opposite of the theoretical value, which is the most common phenomenon in the free market. It is precisely because of this that the interest rate curve is constantly fluctuating. In fact, the system that is madly touted by free market believers is more suitable for stimulating people's fanaticism, and not for suppressing risk. Rationality is always calm, not passionate. Capital is the product of the free market, and has spurred endless desires in the free market, while the digestion of capital redundancy, bonds and other financial products often create more capital. In order to solve such problems, there should be an at least limited neutral balancing role played by a public organization such as a government, especially as it gradually becomes a real social welfare organization and after it turns into an independent public sector.

The Marshall Plan created the miracle of European renaissance after the Second World War[6]. However, if there were no close cooperation between the world's government organizations, it would be impossible to launch such plan. In the 21st century, our world needs more "Marshall Plans" to benefit the world, especially the still impoverished countries and the suffering people; the world needs Marshall Plan-like regional strategic tools. Who then, can properly implement the "Marshall Plans"? The answer can only be government organizations in various countries around the world. Therefore, the proper operation of government organizations in the future world is directly related to global stability and economic health.

We are entering an era of global cooperation.

Finally, there are a few questions that we will discuss in the final parts of this book.

First, the foundation of Piketty's Capital in the Twenty-First Century is the hereditary power of capital. This is a new development in the Neo-Marxist discourse and the basis for his request for the implementation of global capital tax. The hereditary power is still an important academic discovery, but the question is what created hereditary property? What kind of property is Piketty's hereditary property? What is the reason for ensuring that the hereditary property can continue? The answers to these questions are actually in this book; a significant proportion of the hereditary wealth is related to the urbanization movement around the world.

Second, the world must understand the efforts to find new market space; China's New Silk Road & Belt and Road Initiative are all efforts to find new space. The West though, is instinctively suspicions about this. The ideology-based suspicion is understandable, but the world must also note that this effort to find new space for the market also helps to alleviate worldwide capital surplus. It is something that Western politicians do not currently understand[7]. In reality, the economic growth of both China and the United States are related to the African continent; the West will have to face up to the needs and existence of this market space in the future.

Finally, the appreciation of the local currency does not really solve the problems of the world. The renminbi has been subject to excessive appreciation due to international pressure for a long time. Soon, the United States will also face the challenge and pressure of appreciation of its currency. For example, if the United States leads the global floating capital to the U.S. due to the appreciation of the U.S. dollar, it is equivalent to releasing a new version of QE again. The monetary policy that causes the appreciation of the local currency cannot solve the fundamental problem. The global capital surplus is still widespread and becoming more intense. Because a large amount of capital is crowded in narrow channels, it would certainly become more turbulent. In this case, it can be expected that the economic situation in the United States will improve, yet this might just be a superficial illusion. This is because except for the United States, the economy of other countries is unlikely to improve. After complicated transmission, they will eventually suppress the American economy.

What will happen to the future world?

Pessimism is justified for such issue. Our world has entered a clear long-term crisis; it is in an endless cycle and continues blindly without any solution. Can we look back and return to the rational track, relying on the politicians of all countries in the world? This would require the advance efforts in ideology and political goals. But one thing is clear; to truly break free from the tracks of disaster, it is entirely up to the introspection and conscience of the world. This is something philosophical, yet at the same time it is also not philosophical; such the reality of today.

————————————————————————————

[1] Piketty, T., & Goldhammer, A. (2018). Capital in the Twenty-First Century, p. 515.

[2] Author's note: The "Crisis Triangle" is a dilemma of the free markets, and even now there is no real, feasible solution. The fundamental purpose of this book is not to propose solution, but to focus on explaining the relationship between urbanization and global capital surplus, and the possible global market dangers.

[3] Author's note: The policy of Cyprus during times of crisis is also a typical example of "discard and suspension". The Cypriot government's crisis policies are different, but they are basically large-scale freezing, suspension, reversal and write-down of assets. The purpose is to reduce the size of capital and make the crisis within a controllable range.

[4] Meyer, T. & Gunther, T. (1990), Radikale Währungsreform: Deutschland 1948, in Finanzierung und Entwicklung, Vol. 27, No. 1, pp. 6-8.

[5] Chan Kung, "Difang Zhengfu Zhaiwu Guanli Zhidu Chuangxin (Local Government Debt Management System Innovation)". This study originates from China's Ministry of Finance projects. The author believes that the evolution of the government is to become a social public welfare organization to some extent.

[6] The Marshall Plan, officially known as the European Recovery Program, was a U.S. economic initiative to assist in the reconstruction of Western European countries after the end of the Second World War, and had profound impact on the development of Europe and world political pattern. The program was officially launched in April 1948 and lasted for four financial years. During this period, Western European countries accepted a total of US$13.15 billion in aid from the United States, including finance, technology, and equipment, through participation in the Organization for Economic Co-operation and Development (OECD). The author proposes that the Marshall Plan can be regarded as a strategic tool to achieve strategic goals.

[7] Up to now, due to the lack of systematic theory, China has not understood the meaning of the Crisis Triangle, so it only emphasizes the concept of global governance. In terms of market space, it continues to directly collide with the interests of the West, and fails to stand at the height ground to seek for a global consensus and conduct full international consultations.